The November 2024 Endowment Report is now available on karpatkey’s website.

2 Likes

The December 2024 Endowment Report is now available on karpatkey’s website.

3 Likes

The January 2025 Endowment Report is now available on karpatkey’s website.

1 Like

The February 2025 Endowment Report is now available on karpatkey’s website.

karpatkey is pleased to present its first monthly Community Update to the broader ENS Community to increase awareness and transparency of its activities.

Market Update

- February saw heightened volatility across macro and crypto, with persistent trade war concerns and the Fed signalling higher rates amidst inflation concerns.

- The total implied network value (market cap) of the digital asset market stood at $2.92tn at the end of February, down 21% from January (from $3.71tn).

- Over the month of February, BTC is down 17.5%, and ETH is down 32.2%.

- Bitcoin dominance is 59.0%, up 4.1% from January.

- Major market news:

- Bybit hack: Hackers stole over 500,000 ETH, stETH, and mETH ($1.4bn at the time of hack) from Bybit by gaining access to a Safe developer’s computer to control the Safe UI. The broader Bybit hack has shone a light on critical vulnerabilities that can arise from blind signing practices and front-end security.

- FTX began redistributing funds to creditors on February 18; the initial round of distributions included $1.2bn for small claims creditor group (<$50k), recovery ratio is estimated to be ~120% of the account value. Next claims distribution is scheduled for May 30.

- Unichain went live on mainnet on February 11, less than 2 weeks after the launch of Uniswap V4 on January 31. Taken together, the two developments signal a rapid acceleration in new innovation from Uniswap, as Unichain becomes one of the first to host primarily V4-style liquidity.

- Lido announced v3 on February 11, introducing stVaults, which allows stakers to have complete control over the validator set, MEV management, and liquidity access. This can be seen as Lido vying for institutional adoption, especially as a potential provider for staking ETH ETF.

ENS Token Update

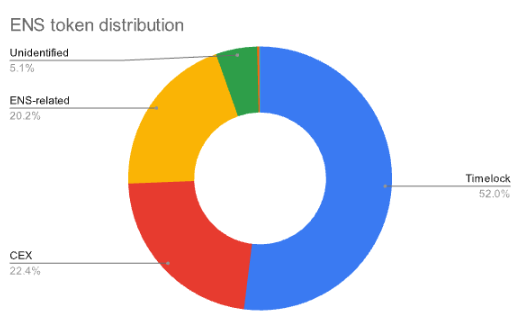

- Token holder distribution for Top 50 ENS token holders remain concentrated in the hands of Centralised Exchanges (“CEXs”) and ENS-Related wallets (DAO, ENS Labs, etc.)

- For further information on ENS Governance and Delegation statistics, please refer to ENS DAO Governance Dune dashboard.

- ENS token price dropped 36.7%, in line with ETH price

- Despite the volatility, trading volume of ENS token also dropped across the venues. Binance’s ENS/USDT daily spot trading volume dropped from ~620k ENS/day to ~509k ENS/day, whilst Upbit’s ENS/KRW dropped from ~1.6M ENS/day to ~1.0 ENS/day; Uniswap v3 ENS/WETH 0.3% trading volume went up from ~38k ENS/day to ~52k ENS/day.

DAO Financial Update

Endowment Update

Please refer to the February karpatkey monthly report for further details.

- Asset Allocation

- AUM of $86M, with capital utilisation ratio of 99.9%

- Endowment Allocation: 72% ETH ($62M), 28% Stablecoins ($24M)

- Yield Generation (“DeFi Results”): $260k gross yield

- Marked-to-market (“MTM”): ENS Endowment’s suffered from $24.2M drawdown in MTM, due to decrease in ETH token price from $3,290 to $2,333.

- Protocol Distribution

- Endowment’s biggest position (protocol exposure) is to Sky/Maker as DAI/USDS continued to offer higher yield vs. USDC in other lending markets. However, Sky/Maker reduced Dai Savings Rate from 11.25% at the start of February to 4.75% at the end of February, resulting in narrowing of the interest rate differential across the lending markets.

- Across the Endowment’s various positions, exposure to each protocol does not exceed 30% of the total Endowment.

For details on the financial accounting, please refer to Financial Reporting Dune Dashboard, as well as the February Steakhouse monthly report.

Other Updates

- Permissions Update #6 for the Endowment has been posted and will be put to vote shortly this month.

- TWAP to procure USDC for the DAO is successfully undergoing execution, and has executed 1,166.67 ETH at an average price of $2,642 for the month of February.

4 Likes

The March 2025 Endowment Report is now available on karpatkey’s website.

kpk is pleased to present its Community Update for the month of March to the broader ENS Community, to increase awareness and transparency of its activities.

Market Update

- March continued to see heightened volatility across macro and crypto, with crypto being whiplashed by macro headlines surrounding trade war / tariffs. Reintroduction of sweeping tariffs has disrupted markets and increased concerns about inflation and recession. The Fed held interest rates unchanged at 4.25%-4.50% and in line its 2025 interest rate projections.

- The total implied network value (market cap) of the digital asset market stood at $2.76tn at the end of March, down 5.3% from February ($2.92tn).

- Over the month of March, BTC showed relative strength, as market prices dipped ‘only’ 2.3% (vs. -6% for S&P 500 Index), while ETH suffered net decreases amounting to 18.4% on the month.

- Bitcoin’s dominance continued to inch upwards, reaching 62.8%, up 3.8% from the end of February.

- Major market news:

- The White House confirmed the issuance of an executive order establishing the long-awaited Strategic Bitcoin Reserve and Digital Asset Stockpile. The stockpile will use tokens (estimated 200k BTC) already owned by the US government. The executive order disappointed some in the market, who had hoped for purchase of new tokens.

- Gamestop announced updates to its Investment Policy, approving Bitcoin as a treasury asset, and completing a $1.5b debt offering, with the proceeds earmarked for strategic purchases of BTC and dollar-denominated stablecoins.

ENS Token Update

- Token holder distribution across the Top 50 ENS token holders remains relatively unchanged, and concentrated in the hands of centralised exchanges (“CEXs”) and ENS-related wallets (DAO, ENS Labs, etc.).

- For further information on ENS Governance and Delegation statistics, please refer to ENS DAO Governance Dune dashboard.

- The ENS token’s price dropped 26.5% in March, outpacing the drawdown in ETH, and therefore resulting in a decline in the ENS/ETH ratio.

- Trading volume continued to drop on CEXs. Binance’s ENS/USDT daily spot trading volume fell 23% from 509k ENS/day to 390k ENS/day, whilst Upbit’s ENS/KRW daily spot trading volume dropped 29% from 1.0 ENS/day to 733k ENS/day.

- Meanwhile, decentralised exchanges (“DEXs”) bucked the trend, as the Uniswap V3 ENS/WETH (0.3%) pool saw trading volume increase an inch (4%) from 52k ENS/day to 54k ENS/day.

DAO Financial Update

Endowment Update

Please refer to the March kpk monthly report for further details.

- Asset Allocation

- Assets under management (“AUM”) of $74.8M, with capital utilisation ratio of 99.9%.

- Endowment Allocation split into 68% ETH ($51M) and 32% Stablecoins ($24M).

- Yield Generation (“DeFi Results”): $232k gross yield generated in March.

- Marked-to-market (“MTM”) valuation: ENS Endowment’s suffered from an $11.2M drawdown in its MTM valuation. This was primarily due to the decrease in ETH token price from $2,333 to $1,826 throughout March.

- Protocol Distribution

- Endowment’s biggest position (protocol exposure) is to Sky/Maker, as DAI/USDS continued to offer higher yield when compared to. USDC in other lending markets. However, Sky/Maker continued to reduce its Dai Savings Rate in March, bringing the rate down from 4.75% at the start of March to 3.5% at the end of March. This resulted in a narrowing of the interest-rate differential across various lending markets, reducing the attraction to DAI/USDS over other assets.

- On-chain yields have been trending lower than off-chain yields throughout March, as US Fed Funds Rate stands at 4.25-4.50%. This is a sign of firmly bearish sentiments across the on-chain economy.

- The Endowment’s introduction of RWA through its upcoming Permissions Update #6 will allow kpk to deploy its assets into RWAs with flexibility, and to take advantage of the difference between on-chain and off-chain yields.

- Across the Endowment’s various positions, no single protocol exceeds 30% of the Endowment’s total exposure.

- Endowment’s biggest position (protocol exposure) is to Sky/Maker, as DAI/USDS continued to offer higher yield when compared to. USDC in other lending markets. However, Sky/Maker continued to reduce its Dai Savings Rate in March, bringing the rate down from 4.75% at the start of March to 3.5% at the end of March. This resulted in a narrowing of the interest-rate differential across various lending markets, reducing the attraction to DAI/USDS over other assets.

For further details on our financial accounting, please refer to Financial Reporting Dune Dashboard, as well as the March Steakhouse monthly report.

Other Updates

-

Permissions Update #6 for the Endowment has been posted, and will be put to vote in the upcoming voting cycle.

-

TWAP to procure USDC for the ENS DAO is undergoing execution, but has been disrupted due to volatilities in the price of ETH. The execution limit price was initially set at $2,062, but the ETH price has subsequently broken firmly below the psychological $2,000 level. In total, 3,000 ETH has been sold at an average price of $2,556. For the month of March, 833.33 ETH was sold at an average price of $2,156.

The April 2025 Endowment Report is now available on karpatkey’s website.

kpk is pleased to present its Community Update for the month of April to the broader ENS Community, to increase awareness and transparency of its activities.

Market Update

- Financial markets were volatile in April, driven by US trade policy and President Trump’s announcement of tariffs that were broader and more punitive than expected. Following an initial, sharp sell-off across risk assets and extreme market volatility (VIX spiked to 60, the highest level since the pandemic), the market recovered through the month. Gold (reached all-time-high of $3,500/oz) and bitcoin shone through the turmoil as the market bidded assets that typically outperform in heightened geopolitical tensions and flush liquidity conditions.

- The total implied network value (market cap) of the digital asset market stood at $3.06tn at the end of April, up 10.6% from March ($2.76tn).

- Over the month of April, BTC showed relative strength, as price gained 14.2% (vs. -0.7% for S&P 500 Index), while ETH ended the month down 1.7%.

- Bitcoin’s dominance retraced slightly, from 62.8% in March to 61.7%.

- Major market news:

- Repeal of the Biden-era crypto tax rule: Trump signed into law a bill to overturn a revised rule from the Internal Revenue Service that expanded the definition of a broker to include decentralised exchanges (DEXs)

- Launch of 21 Capital, backed by Tether and SoftBank, signalled further institutional interest for Microstrategy- type vehicles for Bitcoin exposures. Twenty One expects to launch with more than 42,000 Bitcoin (~$4.2bn), which would make it the third-largest Bitcoin treasury in the world.

ENS Token Update

- Token holder distribution across the Top 50 ENS token holders remains relatively unchanged, and concentrated in the hands of centralised exchanges (“CEXs”) and ENS-related wallets (DAO, ENS Labs, etc.).

- For further information on ENS Governance and Delegation statistics, please refer to ENS DAO Governance Dune dashboard.

- The ENS token’s price increased 17.1% in April, outperforming both BTC and ETH.

- Trading volume showed a mix bag as Binance’s ENS/USDT daily spot trading volume rose 9% from 390k ENS/day to 425k ENS/day, whilst Upbit’s ENS/KRW daily spot trading volume dropped 12% from 733k ENS/day to 647k ENS/day.

- Meanwhile, Uniswap V3 ENS/WETH (0.3%) pool’s trading volume saw an uptick (+6%) from 54k ENS/day to 58k ENS/day.

DAO Financial Update

Endowment Update

Please refer to the April kpk monthly report for further details.

- Asset Allocation

- Assets under management (“AUM”) of $74.1M, with capital utilisation ratio of 99.9%.

- Endowment Allocation split into 67% ETH ($50M) and 33% Stablecoins ($24M).

- Yield Generation (“DeFi Results”): $192k gross yield generated in April.

- Marked-to-market (“MTM”) valuation: ENS Endowment’s AUM was largely flat, with small drawdown of $805k in its MTM valuation.

- Protocol Distribution

- Endowment’s biggest position (protocol exposure) is to Sky/Maker, as DAI/USDS continued to offer higher yield when compared to USDC in other lending markets. However, Sky/Maker continued to reduce its Dai Savings Rate in April, bringing the rate down from 3.5% (at the start of April) to 3% (at the end of April), whilst keeping its Sky Savings Rate steady at 4.5%. This resulted in a narrowing of the interest-rate differential across various lending markets, reducing the attraction to DAI/USDS over other assets.

- On-chain yields have been trending lower than off-chain yields throughout April, as US Fed Funds Rate stands at 4.25-4.50%, signalling bearish sentiments in the crypto space.

- The Endowment will migrate its DAI positions to USDS positions with the passing of Permissions Update #6, which should give a boost to the Endowment returns.

- Across the Endowment’s various positions, no single protocol exceeds 30% of the Endowment’s total exposure.

- Endowment’s biggest position (protocol exposure) is to Sky/Maker, as DAI/USDS continued to offer higher yield when compared to USDC in other lending markets. However, Sky/Maker continued to reduce its Dai Savings Rate in April, bringing the rate down from 3.5% (at the start of April) to 3% (at the end of April), whilst keeping its Sky Savings Rate steady at 4.5%. This resulted in a narrowing of the interest-rate differential across various lending markets, reducing the attraction to DAI/USDS over other assets.

For further details on our financial accounting, please refer to Financial Reporting Dune Dashboard, as well as the April Steakhouse monthly report.

Other Updates

- Permissions Update #6 for the Endowment has been passed

- TWAP to procure USDC for the ENS DAO has been halted due to ETH trading firmly below $2,062, which was the limit price of the TWAP execution. Once the TWAP expires on May 9, 2025, the TWAP will be re-initiated.

- Changes to the Financial Reporting: we have incorporated community feedback with regards to presenting financial statements both with and without $ENS tokens.

- Public Endowment Dashboard: to increase transparency to Endowment activities and performance, we have created a Public Endowment LookerStudio Dashboard; it is still a work in progress, but offers more granular information with regards to the Endowment.

2 Likes

The May 2025 Endowment Report is now available on karpatkey’s website.

kpk is pleased to present its Community Update for the month of May to the broader ENS Community, to increase awareness and transparency of its activities.

Market Update

- The market continued its positive momentum in May as concerns over aggressive tariff threats and trade wars were alleviated, and institutional inflows continued.

- BTC (+12%) reached a new all-time high of $112k mid-month, whilst ETH (+47%) strongly outperformed, firmly reclaiming the psychologically-significant $2k level.

- ETHBTC bounced from local lows of 0.018 and ended the month at 0.02416. May was also marked by a bifurcation of performance across the crypto space; despite strong ETH outperformance relative to BTC, most other altcoins (except for memecoins and HYPE) struggled to outperform Bitcoin (XRP -3%, BNB +10%, SOL +7%).

- The end result was an increase in Bitcoin dominance by 1.82 percentage points (from 61.68% at the start of May to 63.50% at the end of May).

- The total implied network value (market cap) of the digital asset market stood at $3.37tn at the end of May, up 10.4% from April ($3.06tn).

- Despite the general market rally, funding rates (both on-chain and off-chain) and open interest still remained subdued, potentially reflecting higher levels of sidelined capital and/or retail and long-term holders selling. This indicates that such short-term rallies are not yet indicative of a longer-term bullish trend, indicating that caution in approach may still be prudent.

A few interesting developments in the crypto space in May were

- Increasing numbers of entities are copying the Microstrategy playbook (i.e. using financial engineering to purchase Bitcoin or other cryptocurrencies to become crypto treasury companies).

- Strategy (formerly Microstrategy) further entered into sales agreement to issue and sell up to $2.1bn worth of its Preferred Stock.

- Metaplanet (a publicly-listed company on the Tokyo Stock Exchange) announced it will adopt Bitcoin as a strategic treasury reserve asset, citing Japan’s poor macroeconomic environment and a weak JPY as motivating factors. It will be leveraging cheap JPY borrowing costs to issue long-dated JPY liabilities to buy Bitcoin (JPY/Bitcoin carry trade).

- SharpLink (SBET) announced a $425M private placement to initiate a first-of-its-kind Ethereum treasury strategy. SBET rallied from $33.93 to a high of $124, but has since mostly retraced its gains.

- Trump Media (DJT) announced that it will raise about $2.5bn ($1.5bn via shares, $1bn via convertible notes) to invest in Bitcoin as it looks to diversify its revenue.

- Circle filed for public listing on the NYSE under the ticker symbol “CRCL”, with target valuation of up to $6.71bn.

- CRCL opened at $69 on June 5th 2025, and finished its first week of trading at $117.2, making its market capitalisation over $26B. Comparing to on-chain tokens, this valuation would make CRCL a top 10 token by market cap.

Off-chain markets have proven to be exciting. Following the successful initial public offering (IPO) of Circle, we expect more crypto companies to target IPOs in the near future, as investor appetite for crypto stocks increases. Crypto treasury companies have also been getting rewarded for buying Bitcoin, and have outperformed Bitcoin in the last 1 year, leading to a virtuous cycle for the growing number of crypto treasury companies.

However, if this trend reverses and the market stops allocating surplus value to corporations following a strategy of buying crypto (as it did for DJT and Gamestop), corporate demand for Bitcoin may start to dry up. In such circumstances, the premium to net asset value (NAV) of these crypto treasury companies would likely compress eventually, like it did for Grayscale’s premium last cycle. We continue to observe these structural drivers as we formulate our market view, and apply caution in the face of short-term market rallies given the backdrop of a lack of participation and compressing premiums.

ENS Token Update

- Token holder distribution across the Top 50 ENS token holders remains relatively unchanged, and concentrated in the hands of centralised exchanges (“CEXs”) and ENS-related wallets (DAO, ENS Labs, etc.).

- For further information on ENS Governance and Delegation statistics, please refer to ENS DAO Governance Dune dashboard.

- The ENS token’s price increased 12.4% in May, narrowly outperforming BTC (but not ETH). Trading volume for ENS picked up strongly.

- On the CEX side, Binance’s ENS/USDT daily spot trading volume rose 16% from 425k ENS/day to 495k ENS/day, and Upbit’s ENS/KRW daily spot trading volume rose 27% from 647k ENS/day to 779k ENS/day.

- On the DEX side, Uniswap V3 ENS/WETH (0.3%) pool’s trading volume saw a good increase of 27% from 58k ENS/day to 74k ENS/day.

DAO Financial Update

Endowment Update

Please refer to the May kpk monthly report for further details.

- Asset Allocation

- Assets under management (“AUM”) of $94.9M, with capital utilisation ratio of 100.0%.

- Endowment Allocation split into 74% ETH ($71M) and 26% Stablecoins ($24M).

- Yield Generation (“DeFi Results”): $241k gross yield generated in May.

- Marked-to-market (“MTM”) valuation: ENS Endowment’s AUM enjoyed a sharp increase from last month, due to $20.5M increase in its MTM valuation.

- Protocol Distribution

- Endowment’s biggest position (protocol exposure) has been migrated from DAI (in Dai Savings Module) to USDS (Sky Savings Module) after successful passing of Permissions Update #6. Sky Savings Rate currently stands at 4.5%, offering still- higher yields compared to Aave and Compound USDC lending markets, but lower than other lending markets, such as Morpho, Euler, and Fluid.

- LP positions on Curve and Balancer (as well as Convex and Aura) have been yielding below ETH staking rates due to reduced emissions of incentives (in $ terms). As such, those LP positions have been disassembled and the Endowment is holding LST positions instead, reducing a layer of risk.

- Across the Endowment’s various positions, no single protocol exceeds 30% of the Endowment’s total exposure.

For further details on our financial accounting, please refer to Financial Reporting Dune Dashboard, as well as the May Steakhouse monthly report, which now presents financial statements both with- and without $ENS tokens.

Other Updates

- TWAP to procure USDC for the ENS DAO Wallet has concluded successfully. Between Feb 7, 2025, and June 4, 2025, 6,000 ETH was swapped for 15.32M USDC (an average price of $2,553). During this period, the average price of ETH was $2,160, effectively saving the DAO $2.36M through prudent execution.

- The initial TWAP expired on May 9, 2025. As ETH traded below the TWAP limit price of $2,062 from March to May, the TWAP execution was incomplete. When the price of ETH fell, the community endorsed the plan to wait for the price to rebound, instead of setting a new TWAP with a lower limit price. On May 16, 2025, the second TWAP was set and has been successfully completed. Details of the trades can be seen on Cow Explorer, and are detailed below:

- Initial block swap: 1,000 ETH swapped for $2.79M USDC (at average ETH Price of $2,788)

- First TWAP (Order Details: 5,000 ETH swap over 90 days; limit price of $2,062): 2,111 ETH swapped for $5.11M USDC (at average ETH price of $2,423)

- Second TWAP (Order Details: 2,889 ETH swap over 20 days; limit price of $2,062): 2,889 ETH swapped for $7.42M USDC (at average ETH price of $2,568)

- The initial TWAP expired on May 9, 2025. As ETH traded below the TWAP limit price of $2,062 from March to May, the TWAP execution was incomplete. When the price of ETH fell, the community endorsed the plan to wait for the price to rebound, instead of setting a new TWAP with a lower limit price. On May 16, 2025, the second TWAP was set and has been successfully completed. Details of the trades can be seen on Cow Explorer, and are detailed below:

2 Likes

The June 2025 Endowment Report is now available on karpatkey’s website.

There is no extended update this month (replaced by the H1 2025 Review).

1 Like

The July 2025 Endowment Report is now available on kpk’s website.

kpk is pleased to present its Community Update for the month of July to the broader ENS Community, to increase awareness and transparency of its activities.

Market Update

- The crypto market extended its rally in July, marking the fourth consecutive month of positive returns.

- BTC gained+9%, reaching a new all-time high above $123K before settling in the $118–$120K range by month-end. ETH significantly outperformed, surging +52%; it briefly exceeded $4,000 before closing in the $3,780–$3,800 range. Institutional inflows reached $11.2B, with Ethereum-based products attracting nearly $5B and Bitcoin products around $5.5B.

- Bitcoin dominance declined slightly (62.34% to 60.87%) as ETH outperformed other majors; some altcoins did incredibly well (ZORA +702%, SPK +290%, ENA +138%, PENGU +127%). Ethena stood out as the rally was accompanied by an increase in USDe supply ($5.3B to $8.6B) and news of Digital Asset Treasury company for ENA. Other top-20 altcoins also ended the month positive, but underperformed ETH (XRP +45%, SOL +35%, BNB +17%, HYPE +3%).

- The total digital asset market capitalisation reached $3.85T at the end of July, up 12.2% from $3.43T in June.

- Crypto funding rates fluctuated significantly during July without reaching extreme levels:

- Off-chain Funding Rates: BTC and ETH funding rates stayed between 3% and 11% on Binance despite the positive price action. Open Interest for Binance BTC and ETH perps saw an increase (BTC Perps: 110K to 130K, ETH Perps: 2.35M to 2.56M)

- On-chain Funding Rates: On Hyperliquid, the rate fluctuations were much more pronounced; ETH funding moved between 6% and 64%, while BTC funding was between 6% and 47%. Open interest for ETH rose sharply from $1.35B to $4B, driven partly by price appreciation but still materially higher. BTC open interest increased from $3B to $4.5B.

Several notable developments in the crypto space in July were:

- Digital Asset Treasuries continued gaining traction and drove demand for ETH.

- BitMine Immersion Tech (BMNR), targeting to hold 5% of total ETH supply, purchased 300K ETH in July, bringing its treasury to 566K ETH.

- Sharplink (SBET) expanded its ETH treasury from 198K to 361K ETH.

- The Ether Machine (DYNX) and Bit Digital (BTBT) also increased their ETH holdings.

- SEC Chair Paul Atkins unveiled “Project Crypto”, a commission-wide push to modernise securities rules and move U.S. financial markets onchain. The plan replaces subjective Howey tests with clear, rule-based token classification. It creates tiered disclosure requirements based on market cap and trading volume. Safe-harbor provisions for tokenised securities and DeFi activities are also included. The draft rules are expected to come in Q4 2025, with potential final adoption by mid-2026. After years of regulatory uncertainty, crypto has a clear path forward.

As noted in previous updates, crypto treasury companies have been rewarded for buying digital assets, outperforming the broader market in the medium term. This has created a virtuous cycle, attracting more participants and driving some further along the risk curve.

However, we remain concerned that if this trend reverses and the market stops allocating surplus value to corporations following this strategy, corporate demand for crypto could dry up. In such circumstances, the premium to net asset value (NAV) of these crypto treasury companies would likely compress, as seen for Grayscale’s premium last cycle. This dynamic remains an important market signal, and we are monitoring it closely as part of our treasury outlook.

ENS Token Update

- Token holder distribution across the top-50 ENS token holders remains relatively unchanged, and concentrated in the hands of centralised exchanges (‘CEXs’) and ENS-related wallets (DAO, ENS Labs, etc.).

- For further information on ENS Governance and Delegation statistics, please refer to ENS DAO Governance Dune dashboard.

- The ENS token’s price increased 37.7% in July, outperforming BTC but lagging behind ETH.

- Trading volume for ENS rose significantly. On the CEX side, Binance’s ENS/USDT daily spot trading volume almost doubled from 333K ENS/day in June to 653K ENS/day in July, and Upbit’s ENS/KRW pair nearly tripled from 474K ENS/day to 1.2M ENS/day.

DAO Financial Update

Endowment Update

Please refer to the July kpk monthly report for further details.

- Asset Allocation

- Assets under management (AUM) of $127.8M, with a capital utilisation ratio of 100.0%.

- Endowment Allocation split into 77.5% ETH ($99M) and 22.5% stablecoins ($28.7M).

- Yield Generation (“DeFi Results”): $312.6K gross yield generated in July.

- Marked-to-market (“MTM”) valuation: increased by $34M, driven by the rise in ETH price.

- Protocol Distribution

- Endowment’s biggest position (protocol exposure) consists of staked ETH in Stader and Stakwise v3 each comprising about 24% of total funds. On the stablecoin side, sUSDS (Sky Savings Rate) is the highest allocation complemented by small allocations to Compound v3 and Aave v3. Morpho lending markets which have been generally comparable or higher than Sky Savings Rate will be introduced in the next permissions update request.

- Across the Endowment’s various positions, no single protocol exceeds 30% of the Endowment’s total exposure.

For further details on our financial accounting, please refer to Financial Reporting Dune Dashboard, as well as the July Steakhouse monthly report, which now presents financial statements both with- and without $ENS tokens.

Other Updates

- Starting July 24th, the Endowment started rebalancing by selling ETH. ~1,142 ETH were sold in July at an average price of ~$3.77k, netting ~$4.3M in stablecoins, which were deployed into yield-generating strategies.

2 Likes

ENS Monthly Community Update - August 2025

The August 2025 Endowment Report is now available on kpk’s website.

kpk is pleased to present its Community Update for the month of August to the broader ENS Community, to increase awareness and transparency of its activities.

Market Update

The digital asset market closed August on a strong note, with both BTC and ETH reaching new all-time highs (ATHs).

- BTC (-4.5% for the month) reached a new ATH of $124.12k mid-August, before retracing to close the month at $108.41k. ETH (+18.4% for the month) outperformed the broader market, peaking past $4.95k before closing the month at $4.38k.

- Institutional inflows slowed down to $4.37B, driven by growing adoption of ETH-based products ($3.96B), but partially offset by outflow from BTC-products (~$301M).

- Bitcoin dominance declined further (from 61% to 58%), driven by strong ETH outperformance. Some exchange-related tokens also made strong gains (OKB +262%, CRO +113%, MNT +67%, KCS +38%). OKB was up sharply after OKX announced the token supply will be cut in half. CRO was up on news of a new digital asset treasury company that will hold CRO, established in partnership with the Trump family. Other strong performers were LINK +48%, POL +43%, PUMP +36% and ARB +36%.

- The rest of the Top 20 digital assets by market cap showed mixed returns, with most underperforming ETH (XRP -5%, SOL +23%, BNB +13%, HYPE +3%).

- The worst performers for the month were BONK -17%, PENGU -16% and surprisingly SKY -16% as it failed to capitalize on the wider stablecoin narrative in August.

- The total implied network value (market cap) of the digital asset market stood at $3.84tn at the end of August and was largely flat for the month.

- Crypto funding rates fluctuated significantly during August without reaching extreme levels:

- Off-chain Funding Rates: Both BTC and ETH funding rates stayed between 5% to 12% on Binance despite choppy price action. Open interest for Binance BTC and ETH was almost flat (BTC Perps: 130k to 131k (BTC), ETH Perps: 2.56M to 2.64M (ETH))

- On-chain Funding Rates: On Hyperliquid, the rate fluctuations were much more pronounced; ETH funding moved between -6% and 38%, while BTC funding was between 5% and 38%. Interestingly, open interest for ETH and BTC was almost equal at $3.70B towards the end of the month.

Several notable developments in the crypto space during August were:

- Digital asset treasuries continued gaining traction, driving ETH demand.

- Tom Lee’s BitMine Immersion Tech (BMNR), which is targeting to hold 5% of total ETH supply, bought almost 1.30M ETH in August, and finished the month with a total of 1.80M ETH in their treasury.

- Sharplink (SBET) also continued to stack their ETH treasury, growing from 361K to 798K ETH.

- Other companies like The Ether Machine (DYNX) and ETHZilla Corporation (ETHZ) also followed suit. The total ETH held by public companies is now a staggering amount of 3.5M ETH or about 3% of the total token supply.

- In a landmark shift, the Commodities Futures Trading Commission announced that spot crypto asset contracts can now be traded on futures exchanges under its jurisdiction—ushering in enhanced federal-level clarity and collaboration with the SEC under “Project Crypto.”

- BlackRock crossed $100 billion in crypto holdings. As of August 14, BlackRock has accumulated approximately $104.00B in crypto assets, with Bitcoin comprising the lion’s share—underscoring a massive institutional commitment to digital assets.

- Crypto enters U.S. retirement plans as a Trump administration executive order now permits 401(k) and other retirement plans to invest in cryptocurrency investment vehicles, private equity as well as other alternative investments, potentially opening trillions in new capital flows, while raising concerns about risk for ordinary savers.

As we pointed out in last month’s report, many digital asset treasury companies are now trading below a multiple of net asset value (mNAV) of 1, meaning the market values these companies below their net asset value. This suggests that the frenzy of DAT may begin to slowly fizzle out, potentially leading to the drying up of corporate demand for crypto. This dynamic remains a vital market signal, and we are monitoring it closely as part of our treasury outlook.

ENS Token Update

- Token holder distribution across the top-50 ENS token holders remains relatively unchanged, and concentrated in the hands of centralised exchanges (‘CEXs’) and ENS-related wallets (DAO, ENS Labs, etc.).

- For further information on ENS Governance and Delegation statistics, please refer to ENS DAO Governance Dune dashboard.

- The ENS token’s price dropped 12% in August, underperforming both BTC and ETH as crypto majors siphoned liquidity from smaller-cap tokens.

- Trading volume for ENS was lower in August as well. On the CEX side, Binance’s ENS/USDT daily spot trading volume fell from 653K ENS/day in July to 481K ENS/day in August, and Upbit’s ENS/KRW volume fell from 1.2M ENS/day to 974K ENS/day.

DAO Financial Update

Endowment Update

Please refer to the August kpk monthly report for further details.

- Asset Allocation

- Assets under management (AUM) of $145.7M, with a capital utilisation ratio of 100.0%.

- Endowment Allocation split into 73.3% ETH ($106.8M) and 26.7% stablecoins ($38.9M).

- Yield Generation (“DeFi Results”): $370.5k gross yield generated in August.

- Marked-to-market (“MTM”) valuation: increased by $18.4M, driven by the rise in ETH price.

- Protocol Distribution

- Endowment’s biggest position (protocol exposure) consists of staked ETH in Stader and Stakwise v3, each comprising about 21% of total funds. On the stablecoin side, sUSDS (Sky Savings Rate) is the highest allocation complemented by small allocations to Compound v3 and Aave v3. Morpho lending markets will be introduced following the next permissions update request, further allowing the Endowment to diversify its protocol distribution.

- Across the Endowment’s various positions, no single protocol exceeds 30% of the Endowment’s total exposure.

For further details on our financial accounting, please refer to Financial Reporting Dune Dashboard, as well as the August Steakhouse monthly report, which now presents financial statements both with- and without $ENS tokens.

Other Updates

- Starting July 24th, the Endowment started rebalancing by selling ETH. ~2,486 ETH were sold in August at an average price of ~$4.04k, netting ~$10.04M in stablecoins, which were deployed into yield-generating strategies.

- In total, ~3,63k ETH were sold at an average price of ~$3.95k, netting ~$14,35M in stablecoins.

- Permissions Update Request #6 has been posted on the ENS forum; the permissions update continued to focus on diversification of protocols, and alignment of permissions with evolving market landscape and liquidity.

5 Likes

ENS Monthly Community Update - September 2025

The September 2025 Endowment Report is now available on kpk’s website.

kpk is pleased to present its Community Update for September to the broader ENS Community, to increase awareness and transparency of its activities.

Market Update

The digital asset market consolidated in September following the record highs of August. While volatility remained elevated, major assets saw a rebalancing of flows and relative positioning.

Market Performance

- BTC (+4.85.% for the month) traded lower after failing to reclaim its $124k ATH, closing September at ~$113k. Market sentiment around BTC weakened amid continued outflows from institutional products.

- ETH (-5.68% for the month) remained resilient, briefly testing the $4.7k level before closing the month at $4.11k. ETH remained the top institutional focus, with derivatives activity and treasury accumulation providing strong demand support.

Institutional Flows

Public ETF data showed that institutional flows cooled in September, with net inflows of ~$1.4 billion into Bitcoin ETFs, while Ethereum ETFs recorded net outflows of ~$669 million, reversing the prior month’s rotation trend toward ETH.

Market Structure & Dominance

- Bitcoin dominance declined from 58% to 55%, driven by ETH’s continued strength and increased participation in mid-cap assets.

- Exchange-related tokens remained in focus, though returns were more muted than in August: OKB (+22%), CRO (+14%), MNT (+8%), KCS (+5%).

- Other notable movers: LINK (+17%), ARB (+12%), DOGE (+9%), while POL (+3%) and PUMP (+2%) slowed after strong August gains.

Underperformers

Underperformers included BONK (-12%), PENGU (-9%), and SKY (-8%), all of which failed to recover from their losses in August.

Market Capitalisation

The total digital asset market capitalisation closed September at $3.72T, down 3.1% MoM, reflecting BTC’s retracement despite resilience across ETH and select altcoins.

Funding & Derivatives

- Off-chain funding rates (Binance):

- BTC: ranged between 4–9%, with open interest fell from 131 K to 127 K BTC.

- ETH: ranged between 6–11%, with open interest up slightly from 2.64M to 2.68M ETH.

- On-chain funding rates (Hyperliquid):

- ETH: ranged between -4–26%.

- BTC: ranged between 3-24%.

- Open interest remained balanced, with ETH and BTC both near $3.5B in OI by month-end.

ENS Token Update

Token holder distribution across the top-50 ENS token holders remains relatively unchanged, and concentrated in the hands of centralised exchanges (‘CEXs’) and ENS-related wallets (DAO, ENS Labs, etc.).

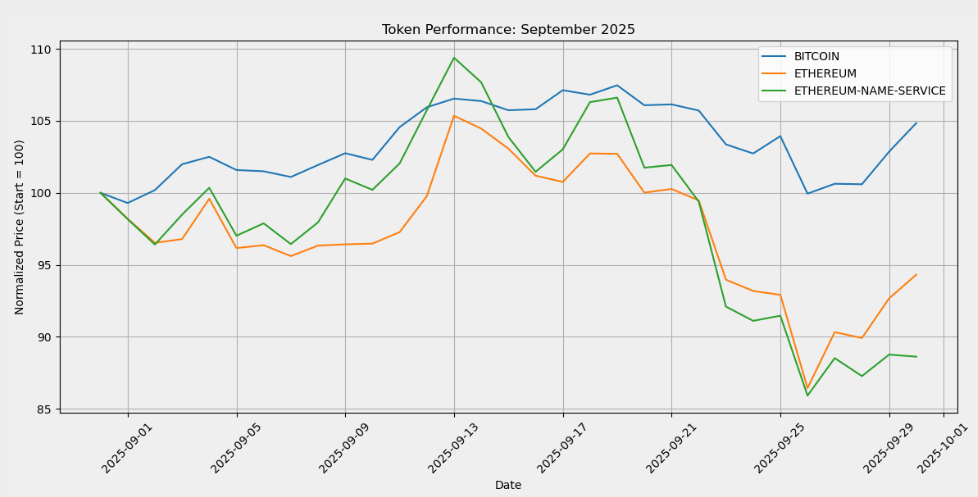

The ENS token’s price dropped -11.38% in September, underperforming both BTC (+4.85%) and ETH (-5.68%) as crypto majors siphoned liquidity from smaller-cap tokens.

Trading activity for ENS declined in September, with total monthly volume reaching 7.68M ENS, equivalent to ~$171.35M. On centralised exchanges, Binance’s ENS/USDT daily spot trading volume fell from 481K ENS/day in August to 256.26K ENS/day in September.

DAO Financial Update

Endowment Update

Please refer to the September kpk monthly report for further details.

-

Asset Allocation

- Assets under management (AUM) of $140.14M, with a capital utilisation ratio of 100.0%.

- Endowment Allocation split into 72.13% ETH ($101.08M) and 27.87% stablecoins ($39.06M).

- Yield Generation (“DeFi Results”): $361.26k gross yield generated in September.

- Marked-to-market (“MTM”) valuation: decreased by $5.79M, driven by the decline in ETH price.

-

Protocol Distribution

- Endowment’s biggest position (protocol exposure) consists of staked ETH in Stader and Stakwise v3, each comprising about 20.41% of total funds. On the stablecoin side, sUSDS (Sky Savings Rate) is the highest allocation complemented by small allocations to Compound v3 and Aave v3.

-

A selection of Morpho markets (cbBTC/USDC (86% LLTV), wstETH/WETH, (96.5% LLTV), wstETH/WETH (94.5% LLTV), WBTC/USDC (86% LLTV), wstETH/USDC (86% LLTV)) will be introduced following the next permissions update request, further allowing the Endowment to diversify its protocol distribution and aim for more attractive yield opportunities.

-

Across the Endowment’s various positions, no single protocol exceeds 30% of the Endowment’s total exposure.

As a complement to our financial accounting, please refer to Financial Reporting Dune Dashboard and September Steakhouse monthly report, which now presents financial statements both with- and without $ENS tokens.

2 Likes

ENS Monthly Community Update - October 2025

The October 2025 Endowment Report is now available on kpk’s website.

kpk is pleased to present its Community Update for September to the broader ENS Community to increase awareness and transparency of its activities.

Market Update

October was a reset month for crypto markets. Risk premia widened across majors, funding conditions softened, and market participants rotated more aggressively into stablecoin positions.

Market Performance

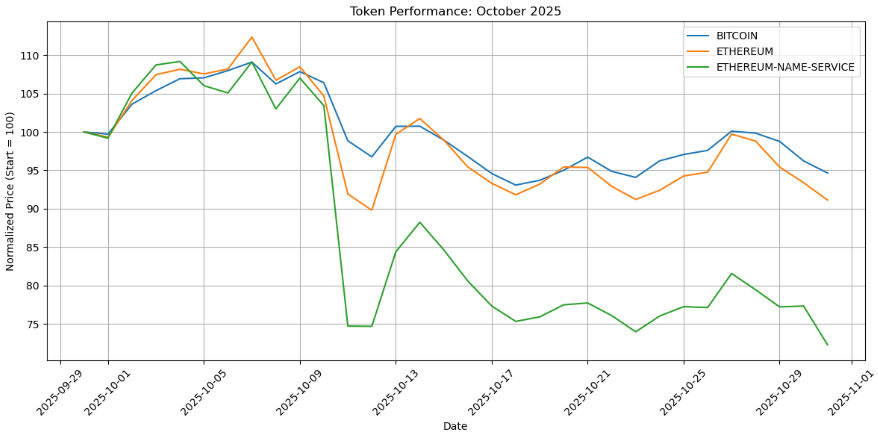

BTC traded lower throughout the month, with spot prices unable to maintain support above $105,000. It closed October at approximately $97,800, down 13.5% month on month. The repricing reflected slower spot ETF flow momentum, reduced marginal buying, and a weaker macro backdrop.

ETH underperformed BTC for a second month, closing October at approximately $3,130, down 23.8% month on month. The liquidation episode on 10–11 October triggered forced unwinds of high-leverage ETH perpetual positions. Liquidations during that 48-hour period accelerated the drawdown, with cascading sell pressure pushing ETH perpetual funding lower and driving double-digit intraday moves across several L1 and L2 tokens, as visible in Hyperliquid onchain perpetual data.

Across the broader market, mid-caps and long-tail assets lagged as traders de-risked into more liquid majors and stablecoins. Exchange-related tokens (OKB, CRO, MNT, KCS) also retraced after several months of prior outperformance.

Institutional Flows

ETF flows weakened materially in October. Bitcoin spot ETFs recorded net outflows of approximately $940M, while ETH spot ETFs saw modest net inflows of $120M (BitMEX Research ETF Tracker). Market makers cited the 10–11 October liquidation window as the point where RFQ volumes and appetite for directional exposure contracted.

Market Structure & Dominance

Bitcoin dominance remained broadly unchanged month on month, holding in the mid-50% range. This indicated that the retracement was systemic rather than a rotation between majors.

Total digital asset market capitalisation closed October at approximately $3.36T, a 9.7% month-on-month contraction, reflecting the repricing across majors and the broader de-risking.

Funding & Derivatives

Funding rates moved lower following the 10–11 October deleveraging event.

Off-chain funding (Binance)

• BTC: ranged 1% to 7%

• ETH: ranged 2% to 9%

On-chain funding (Hyperliquid)

• BTC: ranged –2% to +18%

• ETH: ranged –5% to +22%

Open interest also compressed after the liquidations:

• BTC perpetual OI declined from approximately 127k BTC to 115k BTC by month-end.

• ETH perpetual OI declined from approximately 2.68M ETH to 2.41M ETH by month-end.

ENS Token Update

Token holder distribution among the top 50 ENS holders remained stable in October, with ownership concentrated primarily in centralised exchanges and ENS-affiliated wallets, including the DAO and ENS Labs.

The ENS token declined 27.73% over the period, materially underperforming both BTC, which fell 5.35%, and ETH, which declined 8.88%. The relative underperformance reflected continued rotation from smaller-cap assets into larger, more liquid majors.

Trading activity for ENS strengthened in October, with total monthly volume rising to 12.78M ENS (~$212.65M). On centralised exchanges, Binance’s ENS/USDT spot market saw average daily volumes increase to 412.2K ENS/day, up meaningfully from September levels (256.26K ENS/day).

DAO Financial Update

Endowment Update

Please refer to the October kpk monthly report for further details.

Asset Allocation

- Assets under management (AUM) of $133.37M, with a capital utilisation ratio of 99.9%.

- Endowment Allocation split into 67.63% ETH ($90.09M) and 32.37% stablecoins ($43.17M), in line with the 60/40 mandate and minimum stablecoin runway requirements.

- Yield Generation (“DeFi Results”): $367.22k gross yield generated in October.

- Marked-to-market (“MTM”) valuation: decreased by $7.26M, driven by the decline in ETH price.

Protocol Distribution

- The Endowment’s largest position (protocol exposure) consists of sUSDS (Sky Savings Rate), which accounts for 20.14% of the total funds. On the staked ETH side, staking in Stader (19.96%) and Stakwise v3 (19.76%), continue to be the largest ones.

- Following the approval of permission update #6, the Endowment successfully started to allocate Capital into Morpho markets with the following breakdown:

- cbBTC/USDC (86% LLTV): 2.54M USDC

- wstETH/WETH, (96.5% LLTV): 854.43 WETH ($3.28M as of October 31st)

- WBTC/USDC (86% LLTV): 2.54M USDC

These positions further allow the Endowment to diversify its protocol distribution and aim for more attractive yield opportunities.

- Across the Endowment’s various positions, no single protocol exceeds 30% of the Endowment’s total exposure.

As a complement to our financial accounting, please refer to the Financial Reporting Dune Dashboard and the October Steakhouse monthly report, which now presents financial statements both with- and without $ENS tokens.

1 Like

ENS Monthly Community Update - November 2025

The November 2025 Endowment Report is now available on kpk’s website.

kpk is pleased to present its Community Update for November to the broader ENS Community to increase awareness and transparency of its activities.

ENS Token Update

Token holder distribution among the top 50 ENS holders remained stable in October, with ownership concentrated primarily in centralised exchanges and ENS-affiliated wallets, including the DAO and ENS Labs.

The ENS token declined roughly 20–22% over the month, modestly underperforming both BTC, which fell approximately 17–18%, and ETH, which declined around 21–22%. The relative performance reflects a continuation of the defensive rotation into larger, more liquid assets, with ENS maintaining a similar but slightly weaker trajectory compared to ETH.

Trading activity for ENS softened in November, with total monthly volume reaching 9.38M ENS (~$119.84M). On centralised exchanges, Binance’s ENS/USDT spot market recorded average daily volumes of 312.7K ENS/day, down from October’s elevated activity (412.2K ENS/day).

DAO Financial Update

Endowment Update

Please refer to the November kpk monthly report for further details.

-

Asset Allocation

-

Assets under management (AUM) of $114,40M, with a capital utilisation ratio of 100%.

-

Endowment Allocation split into 61.4% ETH ($70,22M) and 38.6% stablecoins ($44,17M), in line with the 60/40 mandate and minimum stablecoin runway requirements.

-

Yield Generation (“DeFi Results”): $306,40k gross yield generated in November.

-

Marked-to-market (“MTM”) valuation: decreased by $19.7M, driven by the decline in ETH price.

-

-

Protocol Distribution

-

The Endowment’s largest position (protocol exposure) consists of sUSDS (Sky Savings Rate), which accounts for 23.5% of the total funds. On the staked ETH side, staking in Stader (18.2%) and Stakwise v3 (18.0%), continues to be the largest ones.

-

In November, the Endowment continued rebalancing actions to maintain the 60/40 target allocation, resulting in the following adjustments:

-

Migrated $5.1M USDC from Compound to Morpho following risk concerns, bringing total USDC deposits on Morpho to $13.26M.

-

Sold WETH and rETH for $3.49M USDS, which was deployed into Aave to reinforce the stablecoin side of the portfolio.

-

Exited lower-yield USDC positions on Morpho and swapped $2.64M USDC for 883 stETH ( exec price: 2,997.0292 USDC per stETH) to preserve the target split and increase ETH exposure.

-

-

These moves further diversify the Endowment’s protocol exposure and allocate capital toward more attractive yield opportunities.

- Across the Endowment’s various positions, no single protocol exceeds 30% of the Endowment’s total exposure.

kpk published the Permissions Update Request #7 to evolve the diversification of lending markets where the funds can be deployed. The vote is live.

As a complement to our financial accounting, please refer to the Financial Reporting Dune Dashboard and the November Steakhouse monthly report, which now presents financial statements both with and without $ENS tokens.

The December 2025 Endowment Report is now available on kpk’s website.

This monthly update is included in the kpk 2025 Review for the ENS Endowment.

1 Like

ENS Monthly Community Update - January 2026

kpk is pleased to present its January 2026 Community Update to the broader ENS Community, aimed at increasing transparency and awareness around treasury activities.

ENS Token Update

Token holder distribution among the top 50 token holders remained stable in January, with ownership concentrated primarily on centralised exchanges and ENS-related wallets, including the DAO and ENS Labs.

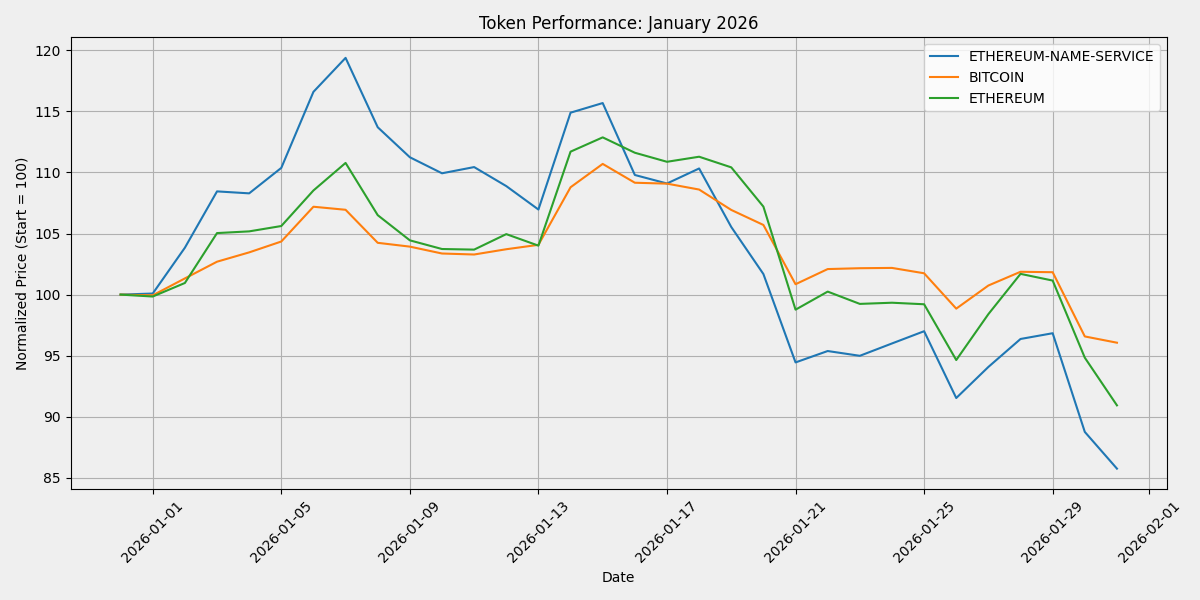

The ENS token declined by approximately 28% over the month, underperforming both BTC, which fell around 11%, and ETH, which declined about 20%. ENS price action largely tracked ETH’s trend, but with slightly weaker performance.

Trading activity for ENS increased in January compared to the previous month, with total monthly volume reaching approximately 7.05M ENS traded ($68.04M). On centralised exchanges, Binance’s ENS/USDT spot market recorded an average daily volume of 227.6k ENS/day, up from December’s activity (166.82k ENS/day).

DAO Financial Update

Endowment Update

Asset allocation:

- Assets under management (AUM) of $102,393,655, with a capital utilisation of 100%.

- Endowment allocation split into 53.5% ETH ($54.8M) and 46.5% stablecoins ($47.5M). The entire crypto market experienced significant volatility, including downward price movements of ETH, at the very end of the month. In early February, following the market turbulence, kpk performed a rebalancing to maintain the 60/40 mandate and minimum stablecoin runway requirements. Similar readjustments will be executed in the forthcoming weeks.

- Yield generation: the Endowment generated $280,181 for the month of January

- Marked-to-market valuation: decreased by $11.47M, driven by the decline of ETH price.

Protocol distribution

The Endowment continues to diversify protocol exposure across 8 distinct protocols, maintaining a balanced distribution between staking and lending strategies.

The largest position remains sUSDC (Sky Savings Rate) at 26.5% of total funds. On the staked ETH side, Stader (16.5%) and StakeWise (16.5%) remain the primary staking exposures.

In January, the Endowment increased allocation to kpk’s curated vault infrastructure, consolidating stablecoin liquidity into actively managed strategies while selectively deploying capital into Compound v3 where yield conditions were temporarily more attractive.

These adjustments:

- Improved yield efficiency across stable/ETH holdings

- Reduced exposure to lower-performing lending markets

Across all positions, no single protocol exceeds 30% of total Endowment exposure, ensuring concentration risk remains controlled.

What’s Next

kpk will facilitate a governance proposal to enable a one-time internal transfer of 2.5M USDC from the ENS Endowment to the DAO timelock, ensuring smooth execution of previously approved funding decisions and maintaining operational continuity without requiring ETH sales.

In parallel, kpk will introduce a new proposal to explore incremental enhancements to the Endowment’s yield strategy within the current IPS framework. The discussion will focus on improving capital efficiency through structured, risk-controlled strategies designed to optimise stablecoin deployment while preserving runway security and mandate alignment.

These initiatives reflect a proactive approach to supporting DAO operations while continuously refining capital efficiency and long-term sustainability.

1 Like

ENS Monthly Community Update - February 2026

Introduction

kpk is pleased to present its February 2026 Community Update to the broader ENS Community, aimed at increasing transparency and awareness around treasury activities.

ENS Token Update

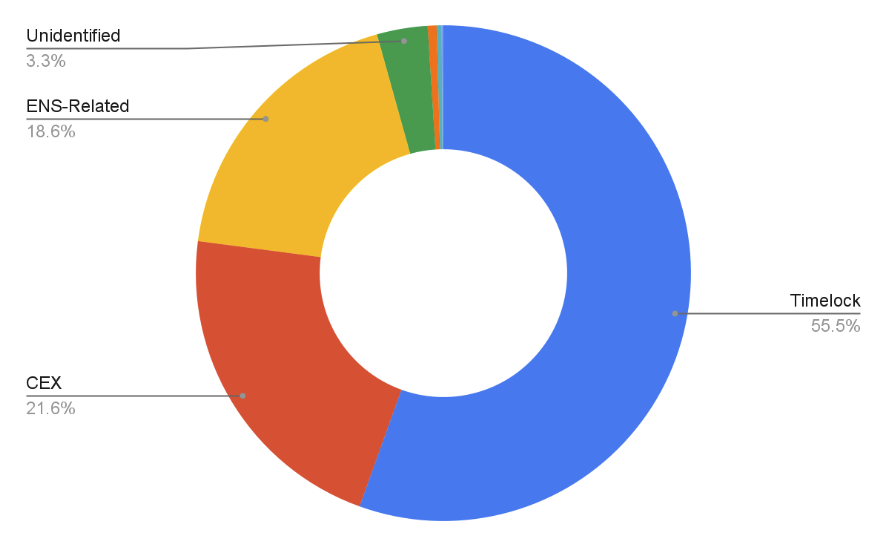

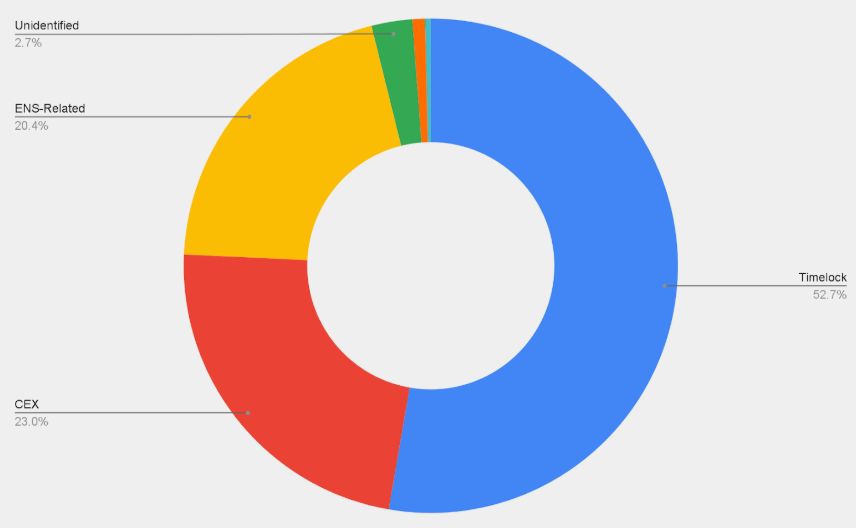

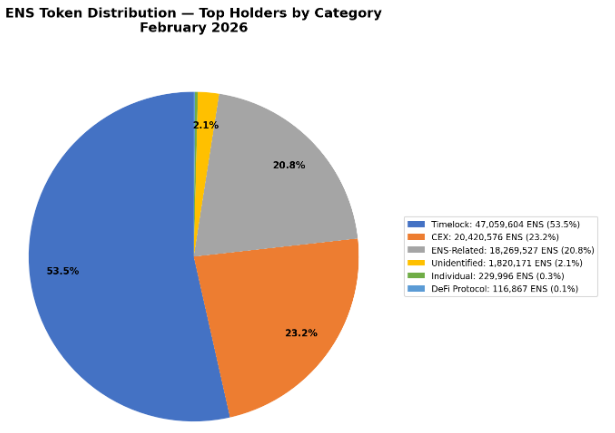

ENS token holder distribution among the top holders remained broadly stable in February, with ownership concentrated primarily in the Timelock contract (53.5%), centralised exchanges (23.2%), and ENS-affiliated wallets, including the DAO and ENS Labs (20.8%). No material shifts in holder composition were observed during the month.

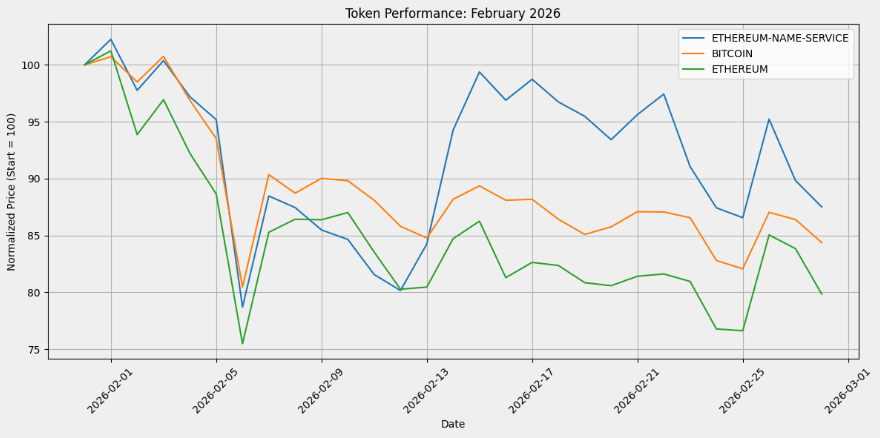

ENS declined 14.6% over February, closing at approximately $5.94 from an opening price of $6.95. This represented a relative outperformance compared to both BTC (-16.4%) and ETH (-19.9%) over the same period. The broader market experienced sustained downward pressure throughout the month, with ENS tracking the general trend but demonstrating marginally greater resilience, particularly during the mid-month recovery around February 13–14.

Trading volume for ENS during February totalled approximately 7 million ENS ($68M) across 28 trading days, with an average daily volume on Binance’s ENS/USDT spot market of approximately 227.6k ENS/day ($2.19M). Trading activity remained stable compared to January.

DAO Financial Update

Endowment Update

Asset allocation:

- Assets under management (AUM) of $89.22M with a capital utilisation of ~97%.

- Endowment allocation split into 55.0% ETH ($49.04M) and 45.0% stablecoins ($40.18M). This is broadly in line with the 60/40 mandate and minimum stablecoin runway requirements.

- Key transactions and rebalancing activities: multiple rebalancing operations were executed during the month to maintain the 60/40 allocation. Allocation changes aimed at optimising yield and remaining within the mandated allocation caps for each protocol were also executed.

- Yield generation: the Endowment generated $218,045 for the month of February.

- Marked-to-market valuation: decreased by approximately $13.16M, driven by ETH price decline of approximately 19.9% over the period (from $2,383 to $1,909).

Protocol Distribution

The Endowment continues to diversify protocol exposure across 7 distinct protocols, maintaining a balanced distribution between staking and lending strategies. The largest position is Sky at 25.0% of total funds. On the staked ETH side, Stader (20.0%) and StakeWise (19.9%) remain the primary staking exposures. Across all positions, no single protocol exceeds 30% of total Endowment exposure, ensuring concentration risk remains controlled.

| Protocol | Allocation % | USD Value | Strategy |

|---|---|---|---|

| Sky | 25.0% | $22.3M | Lending |

| Stader | 20.0% | $17.8M | Staking |

| StakeWise | 19.9% | $17.8M | Staking |

| Aave | 18.4% | $16.4M | Lending |

| Rocket Pool | 9.0% | $8.0M | Staking |

| Morpho | 6.1% | $5.4M | Lending |

| Compound | 1.6% | $1.4M | Lending |

What’s Next

kpk will introduce a new proposal to explore incremental enhancements to the Endowment’s yield strategy within the current IPS framework. The discussion will focus on improving capital efficiency through structured, risk-controlled strategies designed to optimise stablecoin deployment while preserving runway security and mandate alignment.

The initiative reflects a proactive approach to supporting DAO operations while continuously refining capital efficiency and long-term sustainability.

ENS Monthly Community Update - March 2026

Introduction

KPK is pleased to present its March 2026 Community Update to the broader ENS Community, aimed at increasing transparency and awareness around treasury activities.

ENS Token Update

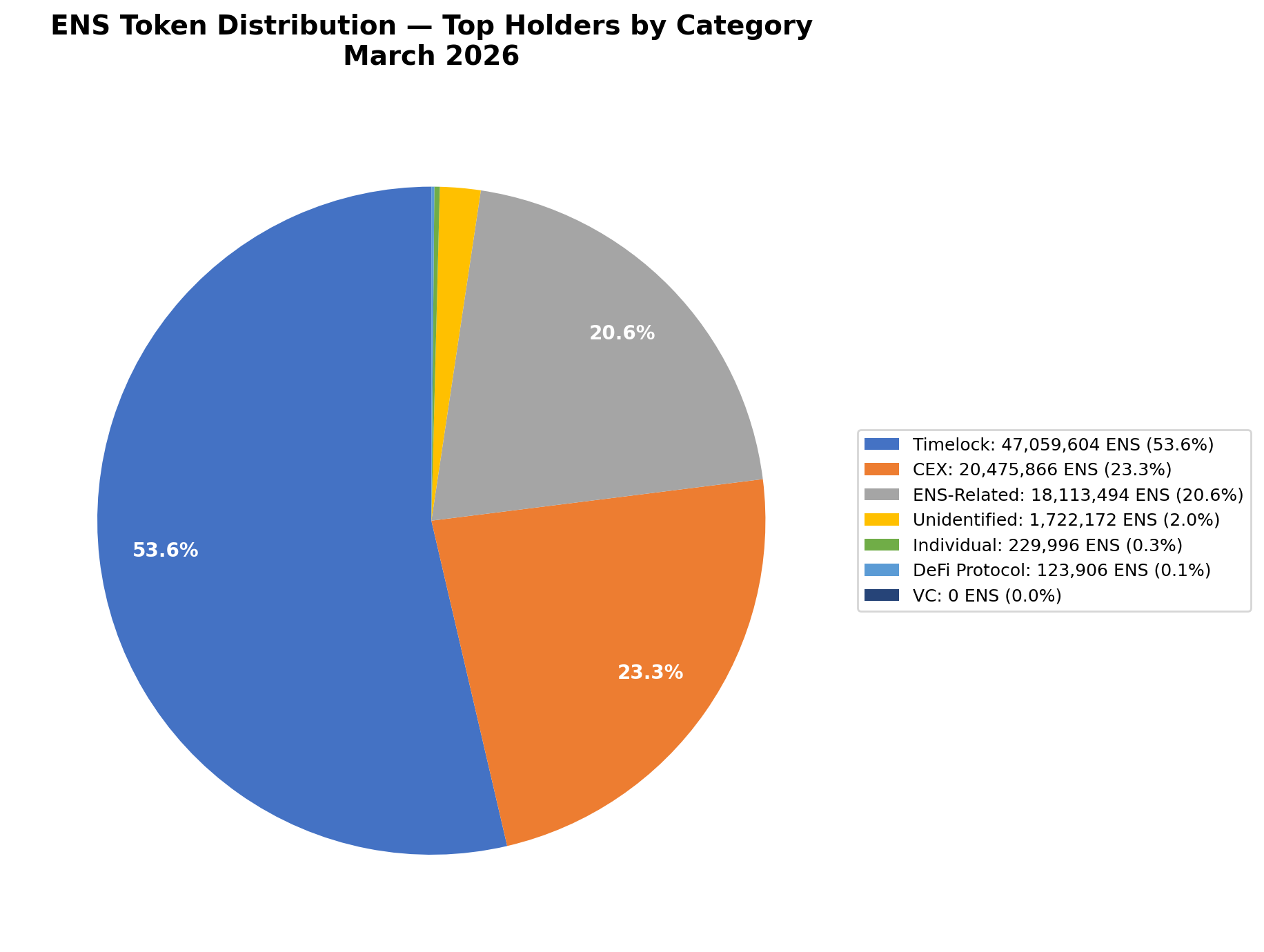

ENS token holder distribution among the top holders remained broadly stable in March, with ownership concentrated primarily in the Timelock contract, centralised exchanges, and ENS-affiliated wallets, including the DAO and ENS Labs. No material shifts in holder composition were observed during the month.

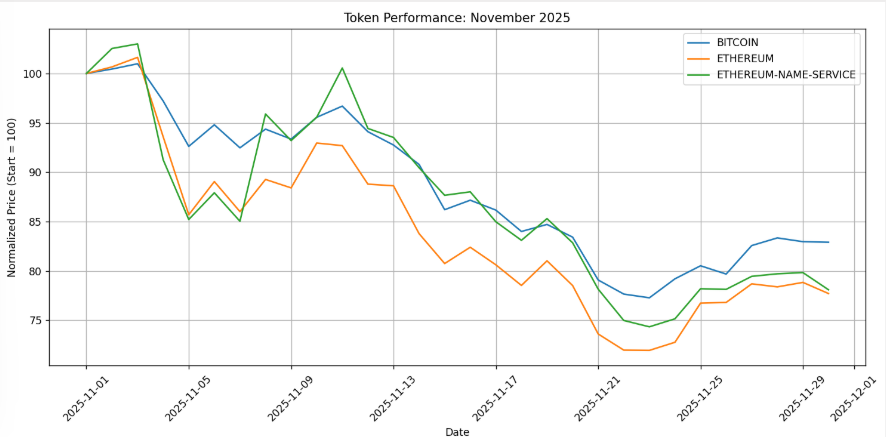

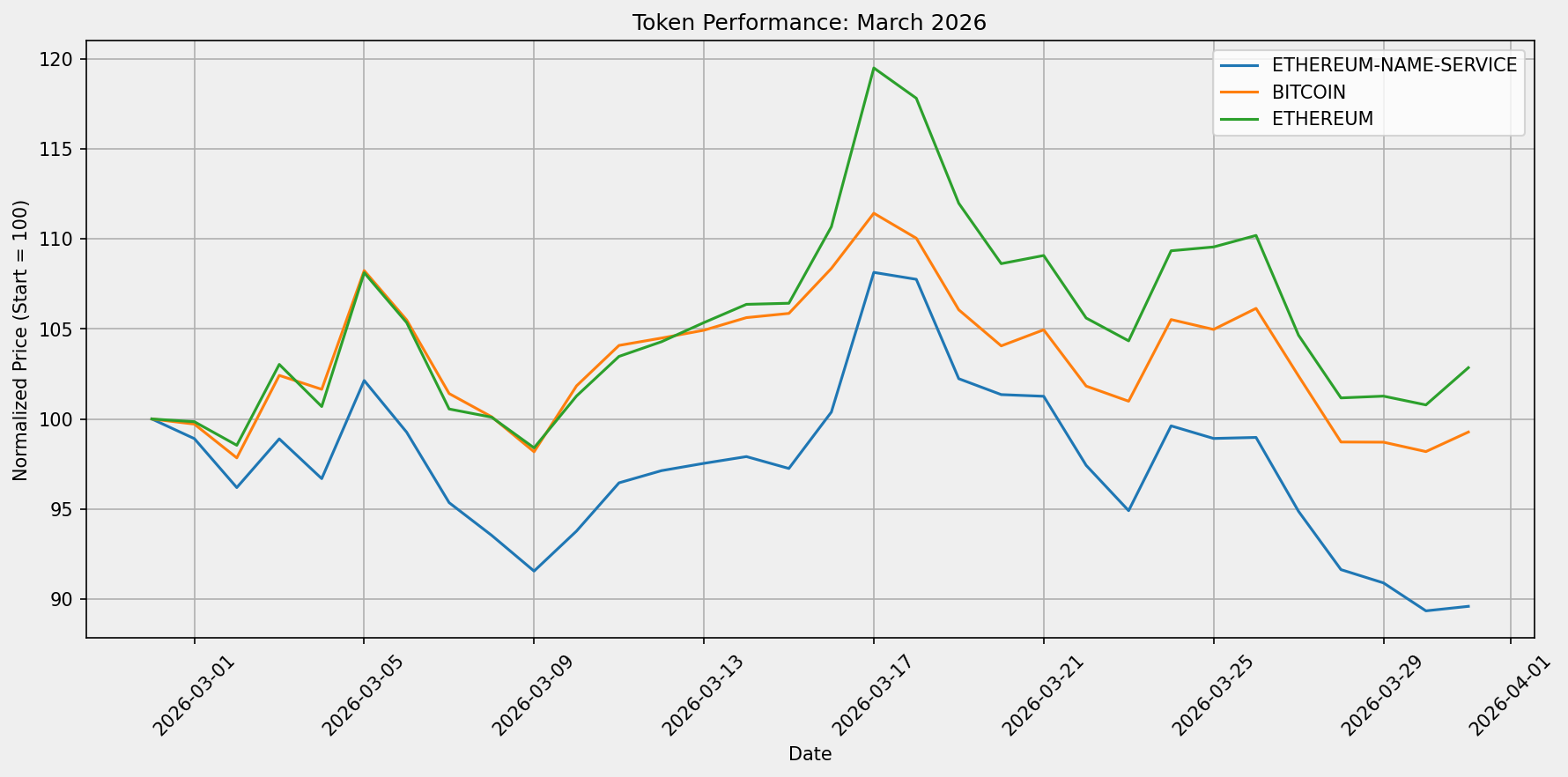

During March, ENS underperformed the broader market. ENS ended the period at 93.0 (indexed from 100), compared to BTC at 99.6 and ETH at 103.0. The underperformance was broadly in line with altcoin weakness across the sector, as ENS declined approximately 7% while ETH posted modest gains of around 3%.

Trading volume for ENS during March totalled approximately 5.67 million ENS ($34.8M) across 31 trading days, with an average daily volume on Binance’s ENS/USDT spot market of approximately 183k ENS/day ($1.1M). Trading activity remained consistent with prior months, reflecting steady but modest market participation.

DAO Financial Update

Endowment Update

Asset allocation:

- Assets under management (AUM) of $91.91M with a capital utilisation of ~100%.

- Endowment allocation split into 57.1% ETH ($52.52M) and 42.8% stablecoins ($39.37M). This is broadly in line with the 60/40 mandate and minimum stablecoin runway requirements.

- Key transactions and rebalancing activities: Multiple rebalancing operations were executed during the month to maintain the target allocation between ETH staking and stablecoin lending strategies, and to guarantee the best risk-adjusted APY.

Additionally, KPK executed operations in response to the Resolv hack that happened on March 22nd. The exposure at risk on the kpk-curated Morpho vault was ~$221k USDC. The full $221k was withdrawn in the same block as a borrower repaid. A depositor redemption cascaded through the vault’s withdraw queue and automatically recovered the full position. No manual intervention, no bot – the vault’s architecture handled the exit on its own. Zero loss to depositors. - Yield generation: the Endowment generated $245,822 for the month of March. That is an annualised APY of 2.9% on the ETH/LSD portion and of 3.7% on the stablecoins portion.

- Marked-to-market valuation: increased by $3,317,452, driven by ETH price appreciation during March, with ETH rising approximately 3% over the period.

Protocol Distribution

The Endowment continues to diversify protocol exposure across 7 distinct protocols, maintaining a balanced distribution between staking and lending strategies. The largest position is Sky at 25.6% of total funds. Across all positions, no single protocol exceeds 30% of total Endowment exposure, ensuring concentration risk remains controlled.

| Protocol | Allocation % | USD Value | Strategy |

|---|---|---|---|

| Sky | 25.6% | $23,526,478 | Usds in ssr (stablecoin yield) |

| Stader | 24.0% | $22,034,205 | Ethx (liquid staking) |

| StakeWise | 23.9% | $21,942,560 | Genesis vault - eth (liquid staking) |

| Aave | 17.0% | $15,590,402 | Lend / borrow (defi lending) |

| Morpho | 5.3% | $4,873,972 | KPK eth prime v2 vault (eth lending) |

| Rocket Pool | 4.0% | $3,665,676 | Reth (liquid staking) |

| Compound | 0.3% | $254,847 | Lend usds (stablecoin lending) |

Other

KPK pushed forward PUR update #8, a routine update to the Endowment Manager’s permissions. Additionally, a one-time withdrawal of 900k USDC from the ENS Endowment’s stablecoin runway was also executed to cover stream payments claimable by ENS Labs.

2 Likes

ENS Monthly Community Update - April 2026

This is the April 2026 Community Update to the broader ENS Community, aimed at increasing transparency and awareness around treasury activities.

The full April monthly endowment dashboard is available on Syncrone.fi.

ENS Token Update

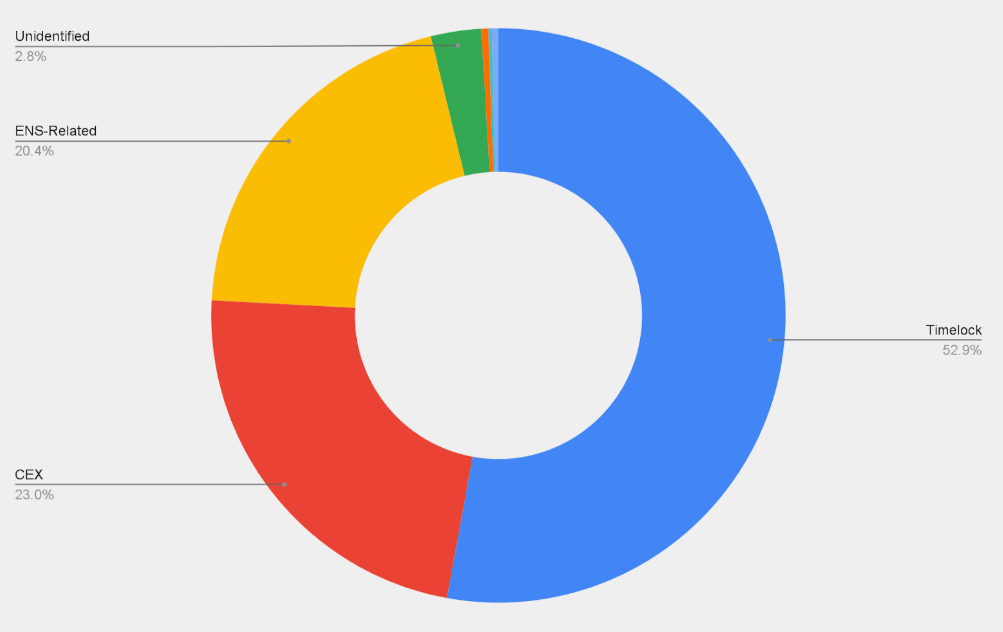

ENS token holder distribution among the top holders remained broadly stable in April, with ownership concentrated primarily in the Timelock contract (~68%), ENS-affiliated wallets including the DAO and ENS Labs (~15%), and centralised exchanges (~14%). No material shifts in holder composition were observed during the month.

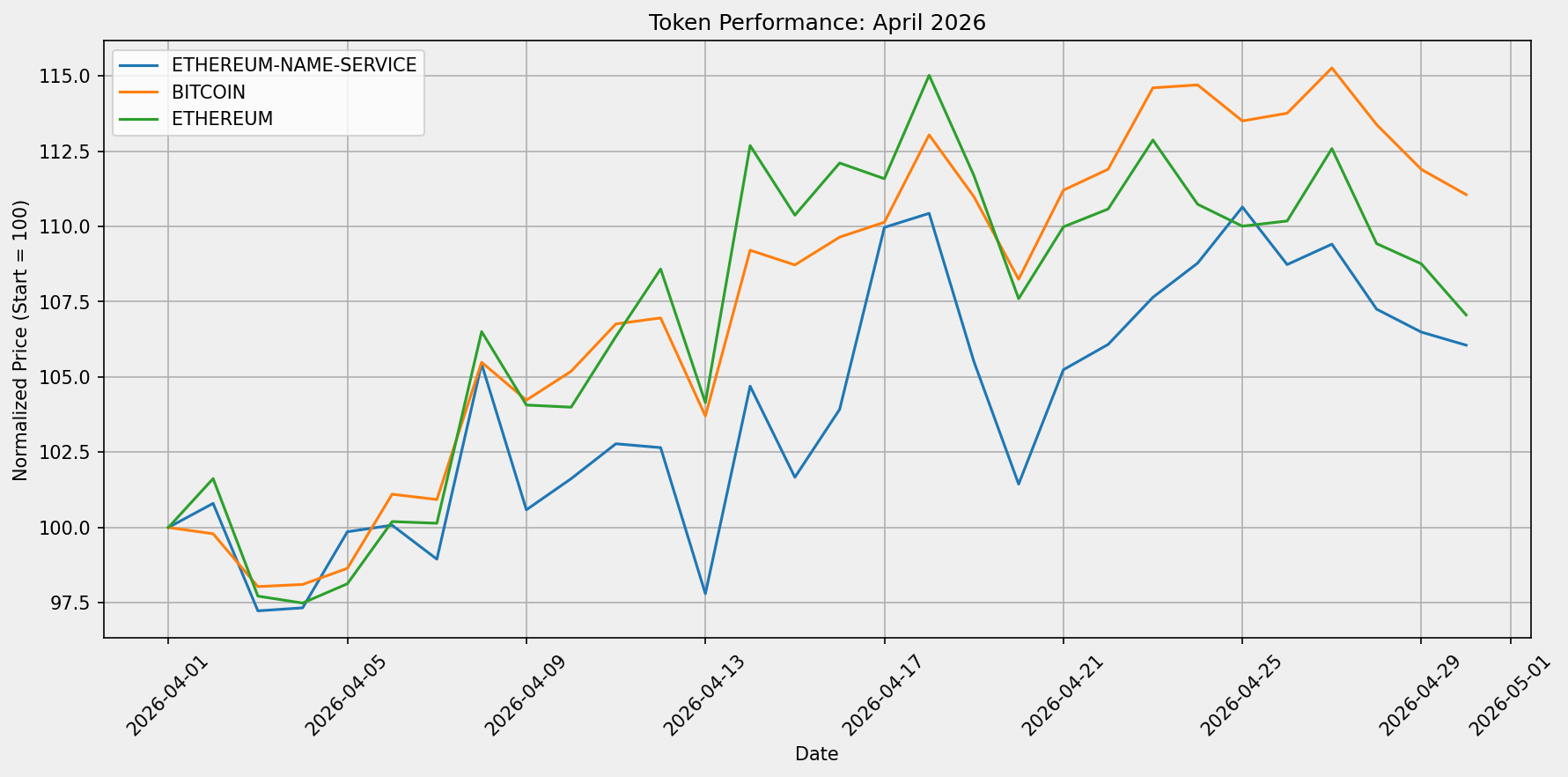

ENS returned +6.1% in April, underperforming both BTC (+11.1%) and ETH (+7.1%) over the period. All three assets appreciated against a constructive broader market backdrop, though ENS lagged the recovery. The chart below shows normalised performance indexed to 100 at 1 April 2026.

DAO Financial Update

Endowment Update

Asset allocation:

- Assets under management (AUM): $93,394,032.93 with a capital utilisation of ~99%.

- Endowment allocation split into ~62.8% ETH (~$58.7M) and ~37.2% stablecoins (~$34.7M). This is broadly in line with the 60/40 mandate and minimum stablecoin runway requirements.

- Key transactions and rebalancing activities: Notably, a ~$4.9M USDC sweep from endowment.ensdao.eth to wallet.ensdao.eth was executed on April 23 to fund DAO operations through end of Q2 2026. This was the final quarterly-style transfer under the prior cadence; beginning in May, treasury flow automation transitions to 6-month runway sweeps using Steakhouse financial data and Meta-Gov coordination. Additional rebalancing operations were executed throughout the month to maintain target allocation and optimise yield across protocols.

- Marked-to-market valuation: increased by $4,444,008.29, driven by broad ETH price appreciation over the period, with staked ETH positions (StakeWise +$1.71M, Stader +$1.72M) and Rocket Pool (+$283k) contributing the majority of gains. Sky (USDS in SSR) contributed +$144k in stablecoin yield.

rsETH Exploit Mitigations: On 18 April, KPK responded to the Kelp DAO rsETH exploit within 20 minutes of the initial alert, executing precautionary exits from Morpho ETH Prime v2 and Aave USDS to eliminate indirect exposure. The ENS Endowment held no direct rsETH; no funds were lost and no bad debt was incurred. Exited funds were held in undeployed ETH for approximately one week before redeployment. Full details are in the ENS governance forum. - Endowment Strategy Return: For the period of April 2026 the Endowment returned $209,000 from strategies managed by KPK

April marked a strong month for the Endowment on a mark-to-market basis, driven primarily by ETH price appreciation. The ~$4.9M USDC sweep to wallet.ensdao.eth on April 23 — the final transfer under the prior quarterly cadence — reflects the transition to the new Treasury Flow Automation system beginning in May.

Protocol Distribution

The Endowment continues to diversify protocol exposure across 6 distinct protocols, maintaining a balanced distribution between staking and lending strategies. The largest position is Sky (USDS in SSR) at 31.8% of total funds (~$29.7M). On the staked ETH side, StakeWise (25.1%) and Stader (25.1%) remain the primary staking exposures, with Rocket Pool contributing a further 4.2%. Morpho accounts for 13.8% across two lending vaults. Across all positions, no single protocol exceeds 32% of total Endowment exposure, ensuring concentration risk remains controlled.

| Protocol | Allocation % | USD Value | Strategy |

|---|---|---|---|

| Sky (USDS in SSR) | 31.8% | $29,659,605 | Lending |

| StakeWise | 25.1% | $23,454,272 | Staking |

| Stader | 25.1% | $23,406,207 | Staking |

| Morpho | 13.8% | $12,863,252 | Lending |

| Rocket Pool | 4.2% | $3,949,118 | Staking |

| Compound | <0.1% | $2,004 | Lending / Staking |

What’s Next

The 2026 Investment Policy Statement (IPS) review is currently underway, with a temp check draft posted to the ENS governance forum for community feedback ahead of a Snapshot social vote. The updated IPS codifies the 60/40 ETH/stablecoin target, formalises a three-year stablecoin runway floor (~$49.3M), and introduces a moderate-risk allocation tier. The forum post can be found here: [Temp Check] 2026 Endowment Investment Policy Update.

Additionally, the 2H 2026 Timelock sweep, the first under the new Treasury Flow Automation system, is scheduled to take place before end of this week. The sweep size will be calibrated against the H1 2026 operating run-rate as reported by Steakhouse.

ENS Monthly Community Update - May 2026

This is the May 2026 Community Update to the broader ENS Community, aimed at increasing transparency and awareness around treasury activities.

The full May monthly endowment dashboard is available on Syncrone.fi.

ENS Token Update

ENS token holder distribution among the top holders remained broadly stable in May, with ownership concentrated primarily in the Timelock contract (~52%), centralised exchanges (~25%), and ENS-affiliated wallets including the DAO and ENS Labs (~20%). No material shifts in holder composition were observed during the month.

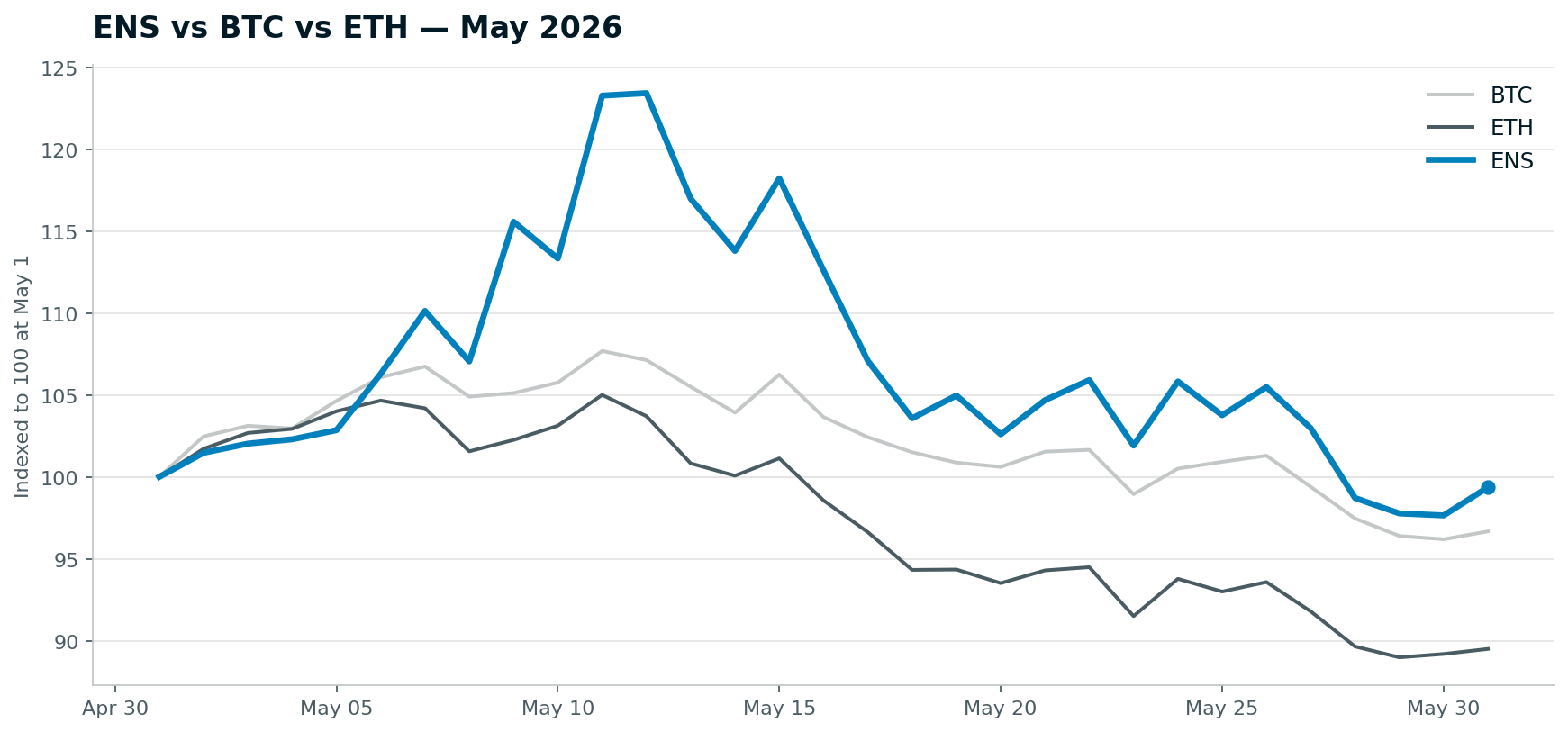

ENS returned −0.6% in May, outperforming both BTC (−3.3%) and ETH (−10.5%) over the period. All three assets declined against a weaker broader market backdrop led by a sharp fall in ETH, though ENS proved relatively resilient and finished the month close to where it started. The chart below shows normalised performance indexed to 100 at 1 May 2026.

DAO Financial Update

Endowment Update

Asset allocation:

- Assets under management (AUM): $86,911,026.98 with a capital utilisation of ~100%.

- Endowment allocation split into ~58.5% ETH (~$50.9M) and ~41.5% stablecoins (~$36.0M). This is broadly in line with the 60/40 mandate and minimum stablecoin runway requirements.

- Key transactions and rebalancing activities: Multiple rebalancing operations were executed throughout the month to maintain the target 60/40 allocation and optimise yield within the mandated allocation caps for each protocol.

- Marked-to-market valuation: decreased by $6,329,691.87, driven by broad ETH price depreciation over the period (ETH −10.5%), with staked ETH positions (StakeWise −$2.62M, Stader −$2.53M) and Rocket Pool (−$440k) accounting for the majority of the decline. Stablecoin positions contributed modest positive yield, led by Sky (USDS in SSR) at +$50k.

- Endowment Strategy Return: For the period of May 2026 the Endowment returned $215,606 from strategies managed by KPK.

May was a negative month for the Endowment on a mark-to-market basis, driven primarily by a broad decline in ETH, which fell approximately 10.5% over the period. Underlying strategy performance remained positive, with the Endowment generating ~$216k in yield across its staking and lending positions, and the 60/40 ETH/stablecoin allocation was maintained throughout the month.

Protocol Distribution

The Endowment continues to diversify protocol exposure across 9 distinct protocols, maintaining a balanced distribution between staking and lending strategies. The largest position is StakeWise at 26.4% of total funds (~$23.0M). On the staked ETH side, StakeWise (26.4%) and Stader (23.4%) remain the primary staking exposures, with EtherFi (4.6%) and Rocket Pool (4.0%) contributing further. On the lending side, the stablecoin allocation is spread across Aave (15.3%), Morpho (12.8%), Sky (10.7%) and Fluid (2.6%). Across all positions, no single protocol exceeds 30% of total Endowment exposure, ensuring concentration risk remains controlled.

| Protocol | Allocation % | USD Value | Strategy |

|---|---|---|---|

| StakeWise | 26.4% | $22,987,218 | Staking |

| Stader | 23.4% | $20,373,879 | Staking |

| Aave | 15.3% | $13,335,934 | Lending |

| Morpho | 12.8% | $11,103,544 | Lending |

| Sky (USDS in SSR) | 10.7% | $9,338,261 | Lending |

| EtherFi | 4.6% | $4,013,286 | Staking |

| Rocket Pool | 4.0% | $3,509,319 | Staking |

| Fluid | 2.6% | $2,249,239 | Lending |

Community Updates

Security update: Zodiac Roles Modifier. In early June, KPK proactively patched a potential issue in the underlying Zodiac Roles Modifier framework (Roles Modifier v2 and Delay Modifier v1.1.0). Our assessment confirmed no impact on the Endowment, and no action is required on the side of ENS — even without the patch, the Avatar Safe permission framework would have prevented the issue from resulting in any loss of funds. Full details are available on the forum here.

2026 Investment Policy Statement (IPS). The 2026 IPS disucssion remains underway. The temp check draft, which codifies the 60/40 ETH/stablecoin target, formalises a three-year stablecoin runway floor (~$49.3M), and introduces a moderate-risk allocation tier, is posted for community feedback ahead of a Snapshot social vote. The discussion can be found here. This will progress to ratification via social vote as soon as practical.

Upcoming Timelock sweep. The Endowment sweep to the Timelock is estimated to executed by KPK within the next two weeks. This will be done in coordination with Meta-Governance. This transfer will move funds to cover DAO operational expenses and streams for the next six months.

1 Like

Introduction

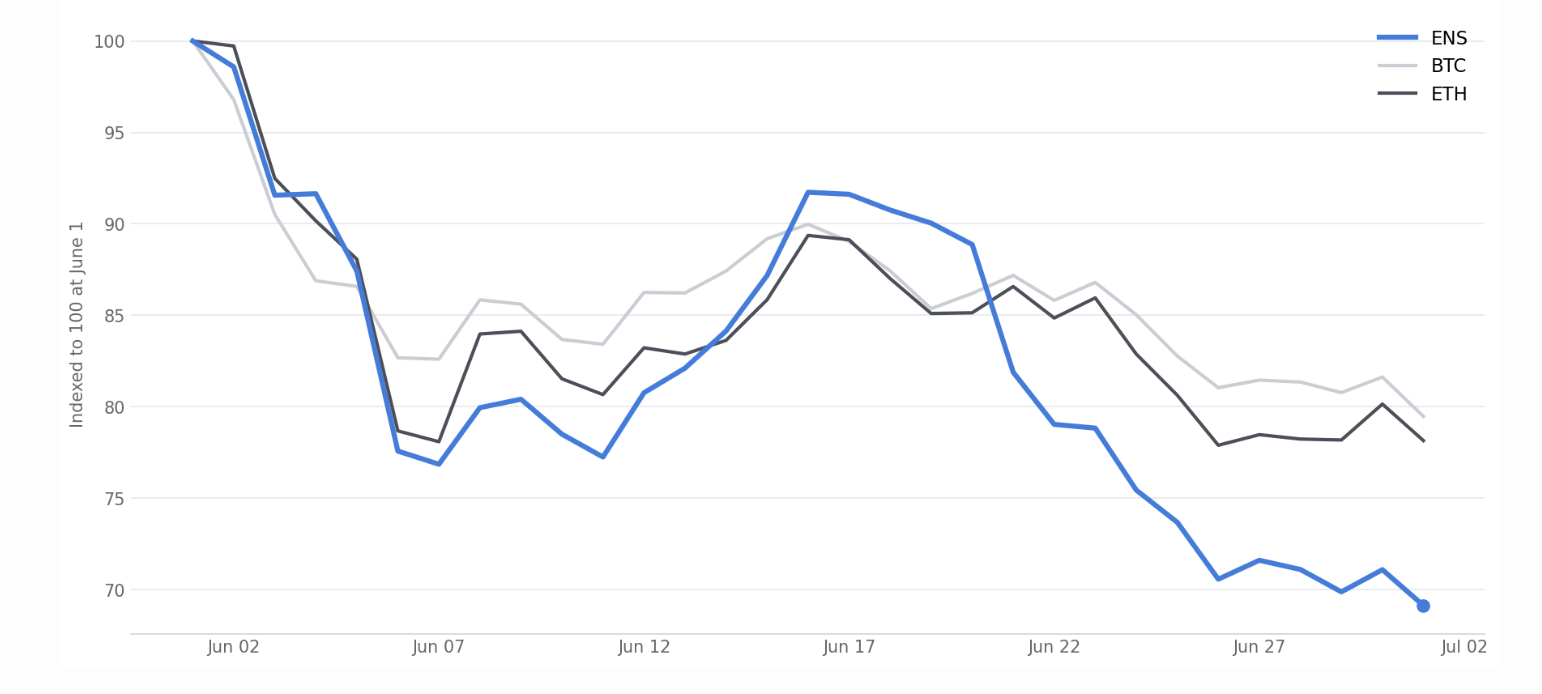

This is the June 2026 Community Update to the broader ENS Community, aimed at increasing transparency and awareness around treasury activities.

ENS Token Update

ENS token holder distribution among the top holders remained concentrated in the Timelock contract (approximately 54% of tracked supply), centralised exchanges (approximately 27%), and ENS-affiliated wallets including the DAO and ENS Labs (approximately 17%) during June. No material shifts in holder composition were observed during the month.

Trading volume for ENS during June totalled approximately 4.9 million ENS ($23M) across 30 trading days, with an average daily volume on Binance’s ENS/USDT spot market of approximately 162.9k ENS/day ($0.77M).

DAO Financial Update

Endowment Update

Asset allocation:

- Assets under management (AUM:) $68.44M with a capital utilisation of ~99.9%.

- Endowment allocation: 60.7% ETH ($41.55M) and 39.3% stablecoins ($26.88M). This is in line with the 60/40 mandate and minimum stablecoin runway requirements.

- Key transactions and rebalancing activities: 44 on-chain transactions were executed across the Endowment’s DeFi positions during June, consistent with routine rebalancing and yield-optimisation activity aimed at maintaining the target allocation and remaining within mandated protocol caps.

- Yield generation: the Endowment generated $175,236 for the month of June.

- Marked-to-market valuation: decreased by $10.82M, driven by an ETH price decline of approximately 21.9% over the period (from ~$2,009 to ~$1,570), which drove an $11.00M negative market impact, partially offset by +$175,236 of positive strategy performance.

Protocol Distribution

The Endowment continues to diversify protocol exposure across 7 distinct protocols, maintaining a balanced distribution between staking and lending strategies. The largest position is StakeWise at 24.1% of total funds. On the staked ETH side, StakeWise (24.1%) and Stader (23.3%) remain the primary staking exposures. Across all positions, no single protocol exceeds 30% of total Endowment exposure, ensuring concentration risk remains controlled.

| Protocol | Allocation % | USD Value | Strategy |

|---|---|---|---|

| StakeWise | 24.1% | $16.5M | Staking |

| Stader | 23.3% | $15.9M | Staking |

| Aave | 16.2% | $11.1M | Lending |

| EtherFi | 13.3% | $9.1M | Staking |

| Morpho | 10.2% | $7.0M | Lending |

| Fluid | 7.8% | $5.4M | Lending |

| Sky | 5.0% | $3.4M | Lending |

Community Updates

- In June the 2026 Investment Policy Statement passed social vote and is pinned on IPFS.

- We opened a discussion, Expanding the Endowment Mandate: Onchain Options, in which we introduce the availability of covered calls for the endowment using Myso or Rysk.