I actually don’t think generalization is necessary for these kinds of proposals. I think if a product team wants to come into a DAO and put the time in to make a proper proposal for why the DAO could benefit from their product, they should be able to shill their product.

You can still have a kind of “fair bid” process where if the DAO decided to engage in this kind of staking, we allow competitors/DAO members to offer their own proposals before making a decision.

It also risks too much indirection (which DAOs are rife with) where proposals basically become “let’s first vote on whether we should vote on this thing we want to maybe do”.

I applaud your initiative of coming to ENS DAO directly and will support this proposal, however, I don’t think Element should be the only fixed yield product employed by the DAO.

In a world where new innovations happen daily, I would be interested in ENS engaging with protocols like APWine or Pendle and creating a diversified fixed-yield strategy. There is a large upside in doing so.

Thanks for your comments! I agree with your viewpoint about how the DAO should aim for safety and diversification, which would in turn foster DAO relationships across the space.

I don’t really see this as a blocker for this proposal and it’s part of why we’ve presented lower allocation options: the DAO can start to activate its treasury now in a safe investment while all the analysis and coordination work for the full treasury management strategy and framework gets built up and put in place.

That said, we can’t speak on behalf of the other protocols mentioned. Our proposed numbers are based on the liquidity that our protocol can support, and what the rates would be if ENS DAO were to enter these positions today.

Request for documentation of Target Market Determination.

Before any voting on appropriateness occurs, I think it would be prudent for the community to request Element Finance produce evidence on who they believe their product/service is suitable for, and a statement to ENS.

Low hanging fruit and worth reaping but consider the side-effects. Some of them have been pointed out and I am sure will be ironed out! Really neat proposal!

@nick.eth apologies, a bit more context would have been helpful.

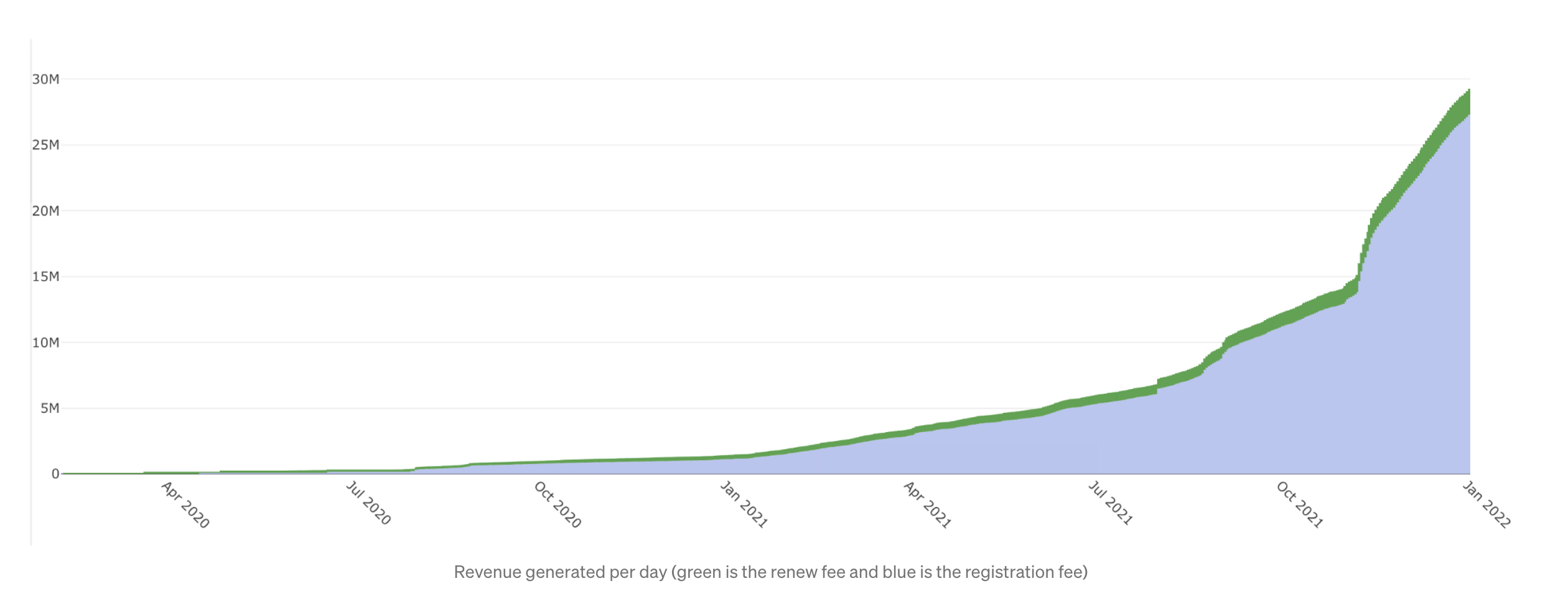

Its a model of revenue as it is at the moment; registrations and renewals made to date, through 2022. A more comprehensive chart summarizing revenue is as follows:

It is clear ENS is great health (nearing almost $30mm in revenue), however highly dependent on new and future registrations.

@Cannabusiness.eth this is free data from Flipside Crypto. We ran a brief bounty program yielding analytics focused on topics such as the airdrop, renewals and registration, and ENS’s revenue.

And @MazyGio, aligned no blocker. Just gauging sentiment - let’s move forward.

I can see that you are trained accountant, and hence I can see how that logic flows in your mind, in other words, cost of capital / opportunity cost / inflation and so on in that fashion. The problem is that as far as blockchain based assets are concerned example of rented house is not applicable. Some of the most popular instruments to generate yield would be using either liquidity pool, staking or “decentralised lending”.

From fund management point of view first two instruments are nothing like “rented house”:

LP carries with it something called “impermanent loss”, which if you ask me is pretty permanent and is just not a very clever way to label that particular part of economics phenomena. I don’t know who coined this term first, but feels like it was some “work in progress” definition which just got stuck and now is incredibly confusing to everyone.

Staking is even worse, because you get exposed to “cross-currency” risk and (lets call it very broadly) “protocol risk”. For example you want to stake Synthetix, then you have to buy SNX and jump through all those smart contract hola hoops, to get that extra yield, once you do that there are 4 variables at play - SNX yield (keep in mind that SNX itself is a very complicated machine) and ETH / SNX / USD exchange rate.

More or less safe option would be decentralised lending on AAVE, but only provided that we use Ethereum market. The reason I’m putting it into safer category is because you are deposit eth, get Aeth in return, on top of that you get yield and no cross currency risk because eth = Aeth. However deposit rate is so small on Ethereum, that I don’t see how this can be effective instrument in the context of ENS fund management. There are other assets which have higher yield, but you get exposed to cross currency risk, protocol risk same as in example above with SNX and in some cases even liquidity risk.

Very broadly speaking these are the 3 classes of yield generating instruments available within DeFi today, I don’t know of any other ways to generate yield.

Investing into real estate and managing portfolio of properties by definition is one of the most conservative approaches towards managing wealth, and frankly its risk profile is nowhere near close to examples above.

To be completely honest, I don’t fully understand this sudden interest to take this capital and plug it into some sort of funky smart contract. Firstly - at the moment ENS doesn’t have any liquidity problems, or cash shortfall, so it’s not like “tomorrow we have to pay those contractors, and because of that we have to squeeze every single penny”. Secondly - reading forum, there are other problems, which require a lot of effort to solve.

I would say the very first question on this long journey which needs to be figured out is how much exactly of free liquidity there is which can be plugged anywhere. There will be some part of capital which will be strictly mandated as “no risk” / “operational stability and security”, and what is left over can be exposed to some more risky / creative ideas. Figuring out amount and structure of “no risk / operational stability” part is the most difficult task at hand and has higher priority.

That’s fair, open to thoughts. I’m not sure there is a

sudden interest to take…

though; evidently this didn’t come across well above, but I’d describe my stance on it as more like “makes sense, some good ideas, needs further research”.

Irrespective of the risks, just sitting on the Treasury permanently - longer term - doesn’t make sense to me as I think we should always try and diversify risk+reward in my view (edit: I’m not saying and didn’t say that was your stance either, for clarity). It’s been laid out above to figure out what type and level of risk is acceptable, and I still think this should go ahead. I’d like to participate to learn more, but suffering a severe lack of available time right now.

I didn’t mean you specifically, I meant in general this whole discussion. I think it’s just that its easiest thing to do - take money and plug it somewhere. But a prudent financial planner in this case should be seeing this as a last priority.

I’m against it. Individual $ENS holders are obviously free to use their tokens however they see fit, but I am completely against outside money managers messing with the treasury funds.

As long as .eth names are selling, and people are still using $ETH, I don’t feel it is necessary to sweep any of the treasury into any kind of vault / LP / yield optimizer / whatever other euphemism that involves locking up or staking $ENS.

I think what he means (and I agree) is that its a prudent approach to move into decision making roles people who are invested into ENS community, that way there is at least some guarantee that decisions made will be carried out in the best interest of ENS rather than self interest.

This is what I’m seeing and saying I’m against. The DAO doesn’t need to allocate a percentage of the treasury to Element Finance or any other vault or money makers. Just my opinion. If individual holders want to, than sure, but I would vote against it being done with the DAO treasury. Just my stance.

Hey Daylon, just to clarify that situation a bit, when he is saying “fixed rate vault”, what that means is that “use one of our products which generates fixed rate” and further he proposes that certain amounts from ENS DAO treasury will be moved into one of those products.

I haven’t done any detailed research on Element Finance, but typically what that means in practice if you look at other products, is that “owner of capital” (O) does not loose control over capital. So even if its moved into one of those products, all that means, is that capital is changing form but control should stay with O.

For example in case of AAVE if you deposit “smartcoin”, you get Asmartcoin in return, which is “control” token, serving as proof that you indeed deposited that amount of smartcoin into protocol, and also serves as sort of “switch” which you pull, if you need to get your smartcoin back.

So they will not be acting as “self-appointed” money managers in technical sense, however should ENS DAO follow blindly that proposal, then it will be the case to a certain extent. This is why it is our role as community members to evaluate proposals, consider alternatives and do due diligence.

I appreciate you spelling that all out for me. I’m pretty experienced with being an LP provider, made thousands holdings a SHIB - ETH 1% pool on Uniswap, and I’m familiar with offerings of services like Curve and AAVE. Again I don’t think this should be something the DAO does with any part of the treasury. If individuals want to utilize their own tokens, I’m all for that. But I think the DAO’s treasury shouldn’t be leveraged anywhere in the form of staking, or LP farming, or interest, or whatever other services are offering to generate an additional yield with the assets. I think registration fees by themselves will provide more than enough capital to operate. If it becomes apparent that that is not the case, then I would be open to options for how else we can utilize and grow the DAO treasury.

Actually I have exactly the same opinion, or very similar at least. Seems like you intuitively understand why this should be the case. But it’s always a good idea to back up your reasoning with solid logic, so that others can see where you are coming from.