1. Weekly Endowment Updates - @kpk + @Steakhouse

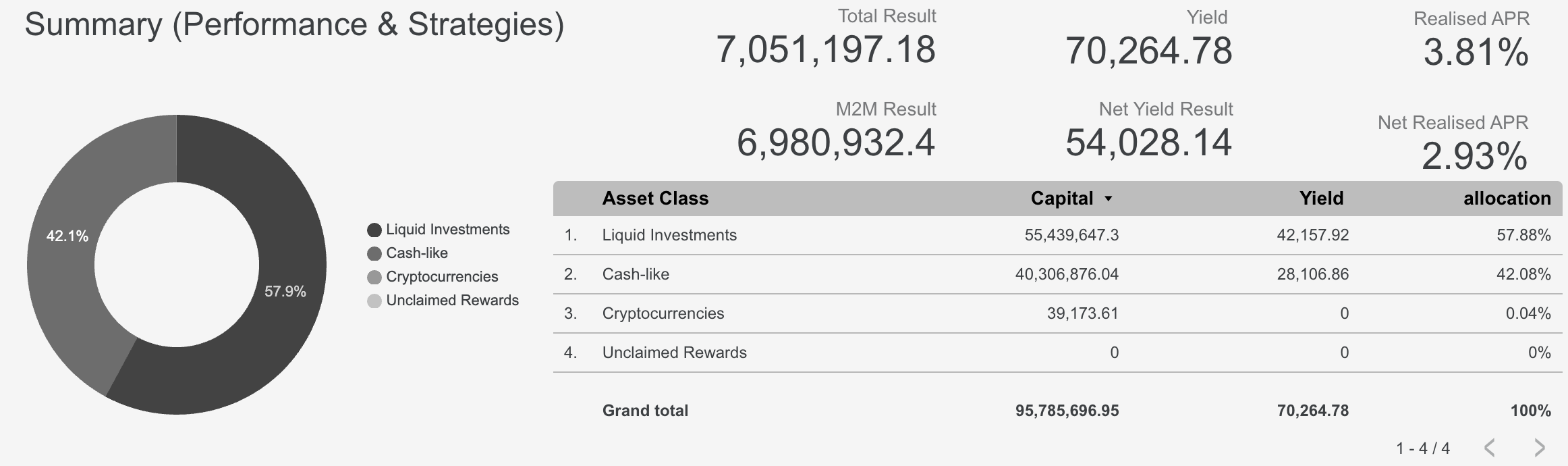

- Endowment at $95M

- 58% in ETH and 42% in stables

- Recent ETH price increase resulted in a total of $7M

- Improved stable allocations APY

- Weekly summary performance for the endowment

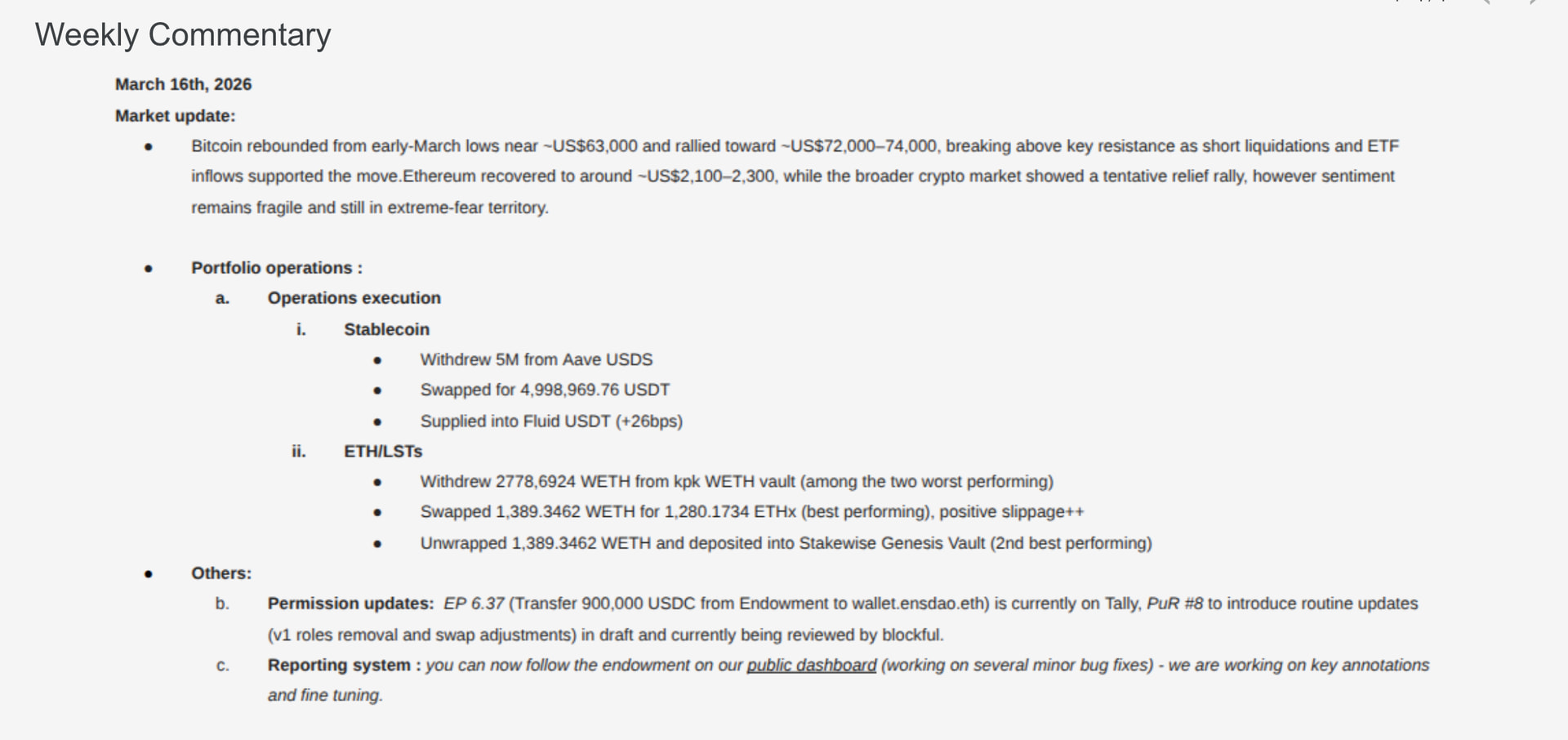

- Full Weekly commentary

- Full weekly report.

- PUR8 will be live soon.

2. Open discussion

2.1. Marcus

- ENS domains posted an article announcing they’re going to stay on L1.

- Since gas is cheap, we can explore ways to subsidize L1 gas costs for all ETH holders

- Marcus proposed Gas Subsidy Contract.

- Problem: ENS collects registration, renewal, and renewal revenue, but there’s no mechanism to return any portion of that value to users.

- Proposed Solution: Retroactive Gas Rebate

- Instead of tracking balances in real time, compute rebates after the fact from public onchain event data.

- Push ETH directly to eligible addresses at the end of the epoch.

- Publish a Merkle Root onchain with a bond and a dispute window of 24-48 hours, where anyone can challenge the amount of ETH being pushed.

- ETH is then distributed automatically to all eligible addresses.

- Open design questions include:

- What’s the right bond amount to avoid griefing?

- What’s the dispute mechanism?

- How to handle batch push execution, given the large number of transactions?

- The complexity of the proposed solution was questioned (Merkle proofs, validator system, etc.) for the problem being solved, effectively returning cents to users per registration.

- Feedback is welcome on the forum about this topic.

2.2. Bojan from Liquity

- Liquity recently wrote a temp check on the forum about creating a more trustless treasury – diversify a small portion of stablecoin holdings or the yield operations into BOLD.

- Liquity issues stablecoins:

- V1 stablecoin: LUSD.

- V2 stablecoin: BOLD.

- Risk profile of LUSD and BOLD is different from that of usual stablecoins.

- Only backed by ETH and Lido ETH

- All contracts are immutable

- No ties to TradFi, no banks, or custodians.

- Traditional stablecoins have direct or indirect exposure:

- Direct exposure: via the backing of a stablecoin.

- Big stablecoins (USDC, USDT) are backed by dollar reserves in a bank.

- Silicon Valley Bank fallout in 2023 caused depegs.

- Indirect exposure: stablecoin backed by other stablecoins.

- Most stablecoins are wrappers or backed by USDC/USDT.

- Partial exposure (20-30%) to USDC/USDT still risky.

- Direct exposure: via the backing of a stablecoin.

- Proposed BOLD as an Alternative.

- BOLD is a stablecoin issued on Liquidity V2.

- Built upon the V1 stablecoin LUSD.

- LUSD has been operational for 5 years with no issues.

- Doesn’t need human interference.

- All contracts are immutable since day one.

- Predictability for treasury managers.

- Always redeemable 24/7 for $1 worth of ETH.

- Even if the market value is lower.

- No ties to TradFi, no banks, no vaults, no custodians, or blacklists.

- Kpk is doing the due diligence currently and will reply to the forum post.

2.3. SPP discussion

- Proposal for a committee model for SPP3 was mentioned as a starting discussion.

- Streams from SPP2 started on May 26th last year.

- Ideally, SPP3 is voted and ready by May.

- There seems to be a consensus on continuing the SPP, but a vote is needed to confirm.

- Need to consider the limited time for discussions and changes.

- Currently, options are:

- Committee model

- 2-tiered approach (up to $300k tier for new teams, and $300k+ tier for established teams)

- Keep the existing one as is.

- James posted “ENS DAO into 2026” to give a more open space for discussion.